Wall Street Is Not Only Rigging Markets, It’s Also Rigging the Outcome of its Private Trials

By Pam Martens and Russ Martens: November 12, 2021 ~

When it comes to sycophants, Wall Street has no shortage of them willing to shill for its egregious private justice system called mandatory arbitration – a system which systematically guts the guarantee of a jury trial under the Seventh Amendment of the Bill of Rights. Think about that carefully, the industry that is serially charged with rigging markets and other felonious acts, is allowed by Congress to run its own privatized justice system. This is something one would expect to find in a banana republic, not in a country that lectures the rest of the world on democratic principles.

Wall Street’s private justice system effectively locks the nation’s courthouse doors to both its workers and customers, sending the claims before conflicted arbitrators who do not have to follow legal precedent, case law or write legally-reasoned decisions.

One of Wall Street’s serial toadies, the U.S. Chamber of Commerce, was quick to release a statement on March 8 when it learned that the House of Representatives was likely to vote on and pass H.R. 963, the “Forced Arbitration Injustice Repeal (FAIR) Act.” (Last week the House Judiciary Committee voted favorably to move the bill out of Committee and on to the full House for a vote. The bill currently has 201 co-sponsors.)

Neil Bradley, Executive Vice President of the Chamber, had this to say in March:

“The U.S. Chamber of Commerce strongly opposes H.R. 963 / S. 505, the ‘Forced Arbitration Injustice Repeal (FAIR) Act’… Members who do not cosponsor this legislation will receive credit for the Leadership component of their ‘How They Voted’ rating.’ ”

If that sounds to you like a threat to members of Congress that they will lose corporate campaign funding if they vote for passage of the bill, you’re thinking along the right lines.

Bradley added this preposterously bogus statement: “Arbitration is a fair, effective, and less expensive means of resolving disputes compared with going to court.”

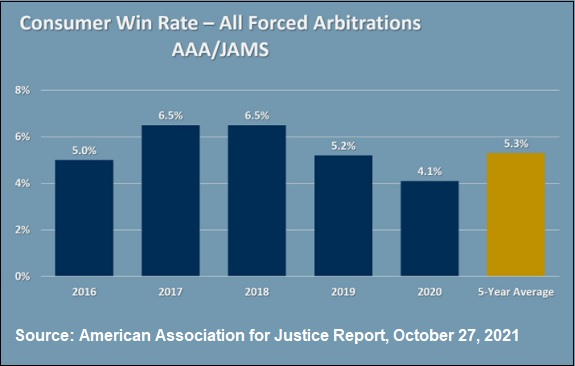

The speciousness of that last statement by Bradley has now been revealed by a study released by the American Association for Justice on October 27. The study found the following:

“In years past, consumers were more likely to be struck by lightning than win a monetary award in forced arbitration. In 2020, that win rate dropped even further. Just 577 Americans won a monetary award in forced arbitration in 2020, a win rate of 4.1% — below the five-year-average win rate of 5.3%. For employees forced into arbitration, the likelihood of winning was even lower. Despite roughly 60 million workers being subject to forced arbitration provisions at their place of employment, just 82 employees won a monetary award in forced arbitration in 2020.”

Wall Street is the only industry in America that has for decades contractually banned both its customers and its employees from utilizing the nation’s courts for claims against the Wall Street firm as a condition of opening an account or getting a job there.

Instead of being able to go to court with a claim of fraud if you’re a customer, or a claim for labor law violations, like failure to pay overtime or sexual harassment if you’re an employee, Wall Street makes its customers and employees sign an agreement to take all such claims into an industry-run or privately-run arbitration system. The above graphic from the study by the American Association for Justice shows how claimants faired in mandatory arbitration forums run by the American Arbitration Association (AAA) and JAMS. The findings cover a broad range of industries, not just Wall Street.

These private justice systems are certainly not fair, and on Wall Street, they are far from cheap. Fees to claimants can run into tens of thousands of dollars as opposed to a few hundred dollars to file in court. Study after study has found that arbitrators most often rule in favor of the corporate interest over the consumer because the arbitrators are financially dependent on repeat business from these corporations.

What Wall Street and its army of lawyers like most about this private justice system is its darkness. Unlike a public courtroom, the press and the public are not allowed to attend the hearings. There are no publicly available transcripts of the hearings as there would be in court. It is next to impossible to bring a court appeal of an arbitration ruling because Wall Street’s biggest law firms have spent decades convincing the courts that these arbitration decisions must be permanently binding.

Another fatal flaw for claimants in these private justice systems is that there is no jury selection from a large public pool of random citizens but rather a repeat-player pool of highly compensated arbitrators.

In September 2007, Public Citizen published a comprehensive 74-page study of mandatory arbitration with a central focus on the National Arbitration Forum. The report is titled “The Arbitration Trap.” Among its findings related to the National Arbitration Forum, Public Citizen found that in California between January 1, 2003 and March 31, 2007 “…a small cadre of arbitrators handled most of the cases that went to a decision. In total, 28 arbitrators handled 17,265 cases – accounting for a whopping 89.5 percent of cases in which an arbitrator was appointed – and ruled for the company nearly 95 percent of the time…Topping the list of the busiest arbitrators was Joseph Nardulli, who handled 1,332 arbitrations and ruled for the corporate claimant an overwhelming 97 percent of the time.”

In 2009, Lori Swanson, the Attorney General of Minnesota, charged the National Arbitration Forum with consumer fraud, deceptive trade practices and false advertising. Swanson’s lawsuit revealed that the National Arbitration Forum was financially shackled to debt collection law firms representing major credit card companies. She provided a detailed roadmap of the financial ties. Less than a week after Swanson introduced her evidence into a court of law, the National Arbitration Forum settled the case by agreeing to stop hearing consumer arbitration cases.

Wall Street’s own industry-run arbitration system also makes good use of the repeat player advantage. On July 20, 2000 the Public Investors Arbitration Bar Association (PIABA) issued a press release accusing the National Association of Securities Dealers (NASD) of rigging its computerized system of selecting arbitrators. The statement read: “In direct and flagrant violation of federal law, the NASD systematically evaded the Securities and Exchange Commission approved ‘Neutral List Selection System’ arbitration rule requiring arbitrators to be selected on a rotating basis. Instead, the NASD secretly programmed its computers to select some arbitrators on a seniority basis – just what the rule was designed to prevent.”

PIABA had discovered the manipulation when a team of its attorneys demanded a test of the selection system at an NASD/PIABA meeting in Chicago on June 27, 2000. PIABA assessed the situation as follows:

“…this rule violation tainted hundreds or even thousands of compulsory securities arbitrations – many still ongoing. In every such instance, the substantive rights of public investors to a neutral panel have been cynically violated. Many public investors were thus twice cheated: first, by an NASD member firm that fraudulently conned them out of their life’s savings, and second by the NASD Arbitration Department’s rigged panels.”

The NASD-run system is now called the Financial Industry Regulatory Authority or FINRA Dispute Resolution Services. For how that’s working out, see Susan Antilla’s 2015 article, “Indicted Lawyers, Peeping Toms Can Wind Up Judges in FINRA Arbitration,” published at TheStreet.com.

A provision of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 required that the newly created Consumer Financial Protection Bureau (CFPB) study the use of mandatory arbitration. As part of the study, the CFPB asked for public comments. This is a sampling of what it heard from those not on the payroll (directly or indirectly) of Wall Street:

“I represent a lot of elderly consumers in elder financial abuse cases. I have numerous situations where arbitration is compelled because they signed an arbitration clause with a bank, agent or brokerage firm. They generally have no idea what they have signed and it is buried in the fine print. I can send you many complaints. These incidents of elder abuse should be litigated in a public place where other consumers can learn about the problems.” – Ingrid Evans, The Evans Law Firm, San Francisco, CA

“Mandatory arbitration has deprived consumers of justice in our country. The presence of the ever-expanding scope of forcing people to arbitrate when they have been tricked or defrauded has damaged our economy more than any other factor. All businesses, from banks to car dealers, that impose arbitration clauses on their customers are then undeterred in their conduct and we suffer. Arbitrators are paid by the companies they sit in judgment of and they are ALWAYS more concerned about whether the company they are judging will select (and pay) them for the next case than justice for the consumer. Please end the scourge of mandatory arbitration.” – Dave Angle, Columbia, MO

“In Public Justice’s experience, the most significant effect of mandatory arbitration clauses in consumer financial services is to dampen and suppress the bringing of claims by consumers. While the civil justice system brings injunctive relief (such as the end of deceptive and misleading practices, the elimination of improperly claimed debts, and the cleaning of credit reports, among other things) and monetary compensation to hundreds of thousands or millions of borrowers each year, only about 1,000 or so consumer cases against corporations of any kind were arbitrated in 2009 and 2010. For a variety of reasons set forth in these comments, the existing evidence that the use of arbitration by lenders suppresses claims – ensures that the vast majority of consumers who suffer legal wrongs will never even try to pursue their rights under federal and state consumer protection laws – is more than adequate for the Bureau to exercise its authority to ban the use of arbitration clauses by all entities within its jurisdiction. The broad data, as well as a number of potent evidentiary records in particular cases, confirms the obvious – that if consumers must each individually pursue their claims in arbitration, lenders will be immunized from liability for all but a tiny proportion of the legal wrongs they may commit.” – F. Paul Bland, Jr., Matthew Wessler, Leslie A. Bailey, Arthur H. Bryant, Amy Radon for the nonprofit organization, Public Justice.

“Among the problems consumer advocates identify concerning the use of mandatory arbitration agreements is the imbalance of power between the drafters of the agreements (i.e., the businesses offering the products and services) and the consumer. This imbalance is particularly acute when mandatory arbitration agreements are included in contracts of adhesion and in transactions targeted at the low-income population.” – Ron Elwood, Legal Services Advocacy Project, St. Paul, MN

It’s long past the time for Congress to stop pretending that it’s studying this charade of a justice system and pass meaningful legislation to reopen the courthouse doors to all Americans.