Why China’s CIPS Matters (and Not for the Reasons You Think)

Payment systems are the plumbing of international finance. As the U.S. and its allies block Russia from a major part of global financial plumbing, China’s Cross-Border Interbank Payment System (CIPS) has been receiving increasing attention. Many observers have wondered whether CIPS and other Chinese channels could provide a replacement not just for trade with China but also for transactions with other countries. For now, this looks like a stretch. But over the long term, participation in CIPS might be an indicator of China’s growing financial power.

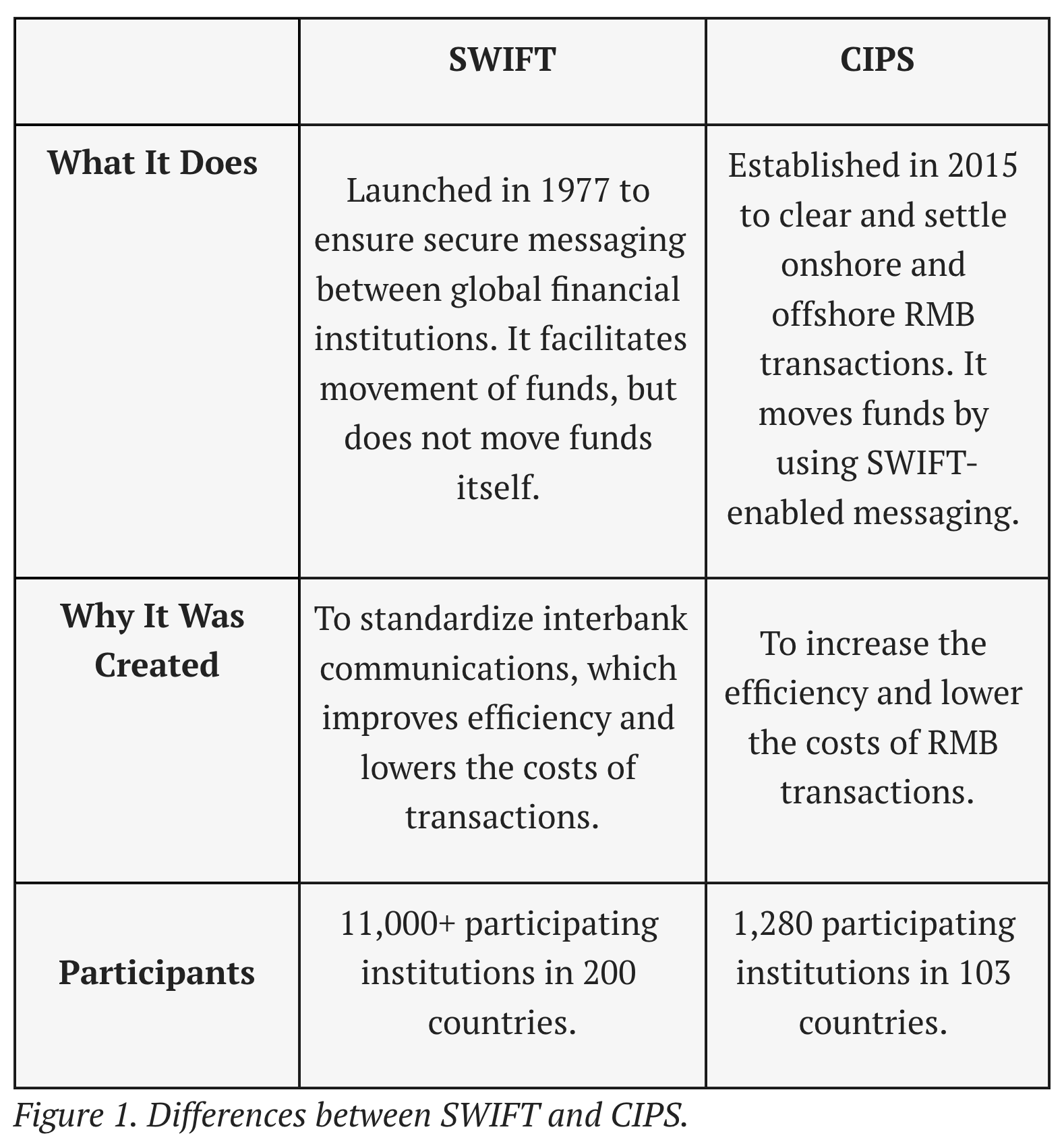

CIPS is not China’s carbon copy of SWIFT (Society for Worldwide Interbank Financial Telecommunication) as they have core technical and contextual differences (see Figure 1). Technically, CIPS clears and settles renminbi (RMB) transactions, whereas SWIFT is a secured messaging protocol that lets banks “talk” to one another. Contextually, CIPS was created to improve the efficiency of RMB transactions, whereas SWIFT was created by institutions from the U.S., the European Union and G-7 countries to enhance global financial messaging.

SWIFT and CIPS play different roles in international finance. SWIFT is a global secured messaging system that allows banks to communicate with each other with high efficiency and low costs. It does not move funds. Instead, it facilitates the secured flow of financial information across borders to support transactions. CIPS, by contrast, is an RMB clearing and settlement mechanism (clearing entails movement of funds from institution A to institution B, and settlement is the finalization of moved funds). In the scenario where user A wants to send funds to user B across borders, there are various options. If their banks are in the SWIFT network, then their banks can communicate with one another via SWIFT codes to complete the transaction frictionlessly. If one of their banks is not in the SWIFT network, then the transaction will need to go through intermediary banks in the SWIFT network, which increases the time and cost of the transaction. CIPS is different from SWIFT, as it is an RMB clearing and settling institution that utilizes SWIFT messaging to facilitate RMB transactions with the rest of the world. China’s CIPS is more similar to the United States’ Clearing House Interbank Payments System (CHIPS), which clears and settles domestic and cross-border U.S. dollar transactions and is plugged into SWIFT for cross-border messaging.

SWIFT and CIPS were created for different purposes. A cooperative of mostly Western banks created SWIFT in the 1970s as a set of standards for international financial messaging. The objective was to ensure collective ease in interbank communication. In contrast, the Chinese government created CIPS to support RMB clearing and settlement on- and offshore, and to aid their objective to make the RMB more attractive. It is narrowly focused on boosting China’s economic and financial prowess. Chinese policymakers started developing the CIPS in 2012, and the mechanism was established in 2015 with SWIFT’s help. China’s stated reason for creating CIPS is to boost RMB internationalization, but with the 2012 SWIFT sanctions on Iran, and the threatened and unimplemented SWIFT sanctions on Russia in 2014, experts in China’s policy community thought establishing CIPS to be even more crucial as a national security imperative. However, China’s promotion for CIPS is also complicated by Chinese policymakers’ determination to limit capital volatility, which conflicts with CIPS’s stated goal of RMB internationalization.

China’s CIPS alone would not help Russia evade the full brunt of U.S. and allied sanctions until the RMB becomes a major player in international finance. While the RMB share of global payments via SWIFT has been rising, the upward trajectory is minuscule, from 1.65 percent in 2020 to 3.2 percent in 2022. And looking at just trade finance for 2022, RMB’s share of global currency in letters of credit and collections is only 1.92 percent, a percentage not proportional to China’s share of the global economy (the U.S. dollar is the first with an 87.38 percent share, and the euro is in second place right before the RMB with a 5.76 percent share). In both finance and trade, even if China continues to provide financial relief to Russia in the international financial system by facilitating currency swaps and approving its RMB-denominated transactions, it does not begin to alleviate Russia’s pain from all sanctions. China-Russia currency swaps are likely not attractive to companies due to the ruble’s excessive volatility. Moreover, because these currency swaps are conducted mostly over RMB instead of rubles, the RMB’s poor convertibility does not ease Russia’s economic pains. The bigger bilateral trade picture is also dim, as China falls behind the European Union when it comes to trade with Russia.

But the U.S. should keep a watchful eye on CIPS because it is a crucial piece of China’s broader ambition in international finance. China’s desire to lead in global finance is a stated goal, most recently enshrined in the Financial Standardization Five Year Plan (2021-2025) released in February 2022. China can lay the groundwork for its ambition by strengthening the efficiency of CIPS, which could pave the way for RMB internationalization, but only if China first makes the whole suite of political and economic structural changes that would make the RMB a safer asset. International trust in the RMB as a safe asset and China as a reliable player in global finance is a necessary ingredient before CIPS can prop up China’s influence in the global financial ecosystem. However, it is still notable that CIPS processed more in 2021 compared to the prior year, with a 75 percent increase in value, and a 50 percent increase in transaction volume (these numbers are sourced from the state-backed newspaper Jiefang Daily, so take this with a grain of salt.) As of January 2022, 1,280 financial institutions in 103 countries and regions have connected to CIPS. While it is a drop in the bucket compared to SWIFT’s 11,000 participants across more than 200 countries, it is not insignificant. Financial policymakers should study the growth in CIPS participation, as it is one indicator of RMB internationalization for China’s potential monetary ascendance.

Chinese policymakers have to contend with a policy paradox—China wants CIPS to be connected to the world yet also be a viable alternative to existing financial institutions. This is because CIPS needs SWIFT to operate in international finance. However, China simultaneously feels the powerful reach of American sanctions. Chinese academics have openly discussed that SWIFT is a point of contention between the United States and Russia. Moreover, China has been collaborating with other countries in providing alternatives to mainstream financial institutions. For example, China has a financial alliance with Russia. In 2010, the two countries agreed to use their currencies to settle bilateral trade instead of using the U.S. dollar. In 2014, the two opened their first currency swap line, which was renewed in 2017 and 2020 with the latest renewal entitling 150 billion yuan over three years. With a 35.9 percent increase in total bilateral trade in 2021, the continuing currency swap would be even more economically important to Russia (although most of China-Russia trade is still settled with the euro). Most recently, the Russian Mir card network is looking to further integrate with China’s UnionPay as Visa and Mastercard suspended their services to Russia. China has been replicating alternative financial arrangements across many other economies in the developing world. If more foreign banks join the CIPS (as either indirect or direct participants), that could be a sign that a China-led alternative channel could become stronger. India-Russia trade, for example, could be an interesting testing ground to watch for CIPS usage, although CIPS’s integration with the rest of the world and other emerging economies is still admittedly nascent.

Policymakers would be remiss not to consider the alternative case, one in which China becomes a more prominent actor in global finance. Imagine a world where blocs have become more defined, where authoritarian countries have become accustomed to working with one another to mitigate the political and economic penalties from international condemnation. There might be just enough competitive pressure for China to make some painful structural changes to its political economic model, such as opening its capital account and embracing financial volatility. This might not happen until long after 2030, but there might be an inflection point where the RMB becomes more attractive and is on the cusp of becoming a more influential currency. At that point, China will have had years to refine its financial plumbing. CIPS and other financial mechanisms and digital innovations native to China could embolden China to contend with current mainstream financial mechanisms such as SWIFT. Then, China will be one step closer to meaningfully countering U.S. and allied sanctions. This is a big if, all contingent on whether China is willing to change its political economic model. Admittedly, China is highly unlikely to do just that in the foreseeable future, as long as the leadership’s calculus around social control and financial stability outweighs its ambition for a more internationalized RMB. However, U.S. policymakers should still keep a close eye on even a mildly successful expansion of the RMB. Because if the RMB becomes a more attractive asset, then CIPS, eCNY, Blockchain-based Services Network (BSN), and many other traditional and emerging financial mechanisms could get China to a position of strength to challenge leaders in the global financial order.