Ukraine: trapped in a war zone

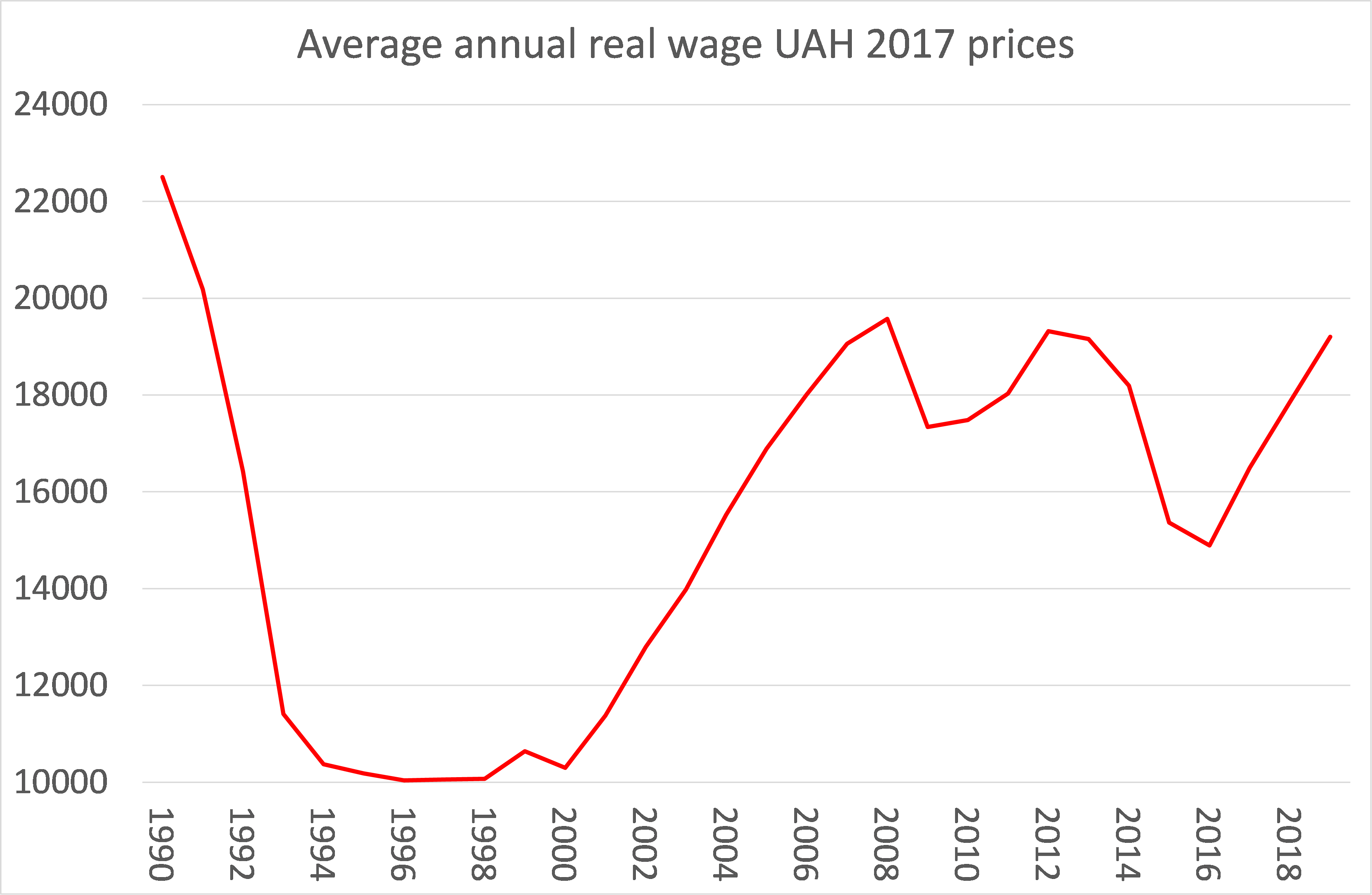

As the drums of war sound for Ukraine, what will be the impact on Ukraine’s economy and the living standards of its 44m population, whether war is avoided or not? I’ve posted on Ukraine several times before during the intense economic crisis that the country experienced in 2013-14 culminating in the collapse of incumbent government, the Maidan uprising and eventually the Russian annexation of Crimea and the predominantly Russian-speaking eastern provinces. The situation was dire for the people then. It improved a little for a while afterwards, but economic growth remains relatively low and living standards have stagnated at best. Average real wages have not risen in 12 years and collapsed severely after the 2014 crisis.

Source: EWPT 7.0 series

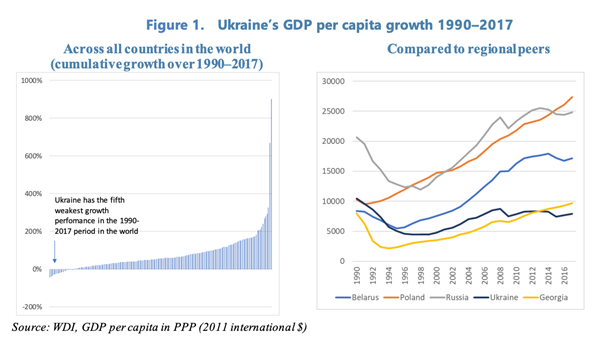

Source: EWPT 7.0 seriesUkraine was the hardest hit by the collapse of the Soviet Union and the ‘shock therapy’ of capitalist restoration in Eastern Europe and Russia itself. All the former Soviet satellites took a long time to recover GDP per head and income levels, but in the case of Ukraine it has never got back to the 1990 level. Ukraine’s performance between 1990 and 2017 was not just worse than its European neighbours. It was the fifth-worst in the entire world. Between 1990 and 2017 there were only 18 countries with negative cumulative growth and even in that select group, Ukraine’s performance puts it in the bottom third along with the Democratic Republic of Congo, Burundi and Yemen.

In the debt and currency crisis of 2014, Ukraine was saved from total meltdown by three things: first, it defaulted on its debt owed to Russia, which (despite much effort) Russia has not been able to recoup so far. Second, post-Maidan governments engaged in series of IMF bailouts; and third, the price for which was a severe programme of austerity in public services and welfare support. Ukraine owes Russia $3bn, or more than 10% of its FX reserves and if paid, would more than double Ukraine’s external financing gap. That gap is being currently filled by IMF funds, while Ukraine ‘negotiates’ with Russia on a ‘debt restructuring’, supposedly mediated by Germany. Ukraine, in breaking with Russian influence from 2014, has chosen to or been forced to rely on the ‘West’ and IMF credit to support its currency and hope for some economic improvement.

IMF handouts continue. The latest is an agreement to extend loans into 2022 worth $700m of a total $5bn IMF ‘stand-by arrangement’. For this money, Ukraine “must keep its debt ‘sustainable’, safeguard the central bank’s independence, bring inflation back into its target range and tackling corruption.” So austerity measures must be applied to public spending; the central bank must act in the interests of foreign debtors and not allow the currency to devalue too much and keep interest rates up without the interference of the government; and the rampant corruption in government with the Ukrainian oligarchs must be controlled. (see IMF Stand-by arrangement November 2021 report. )

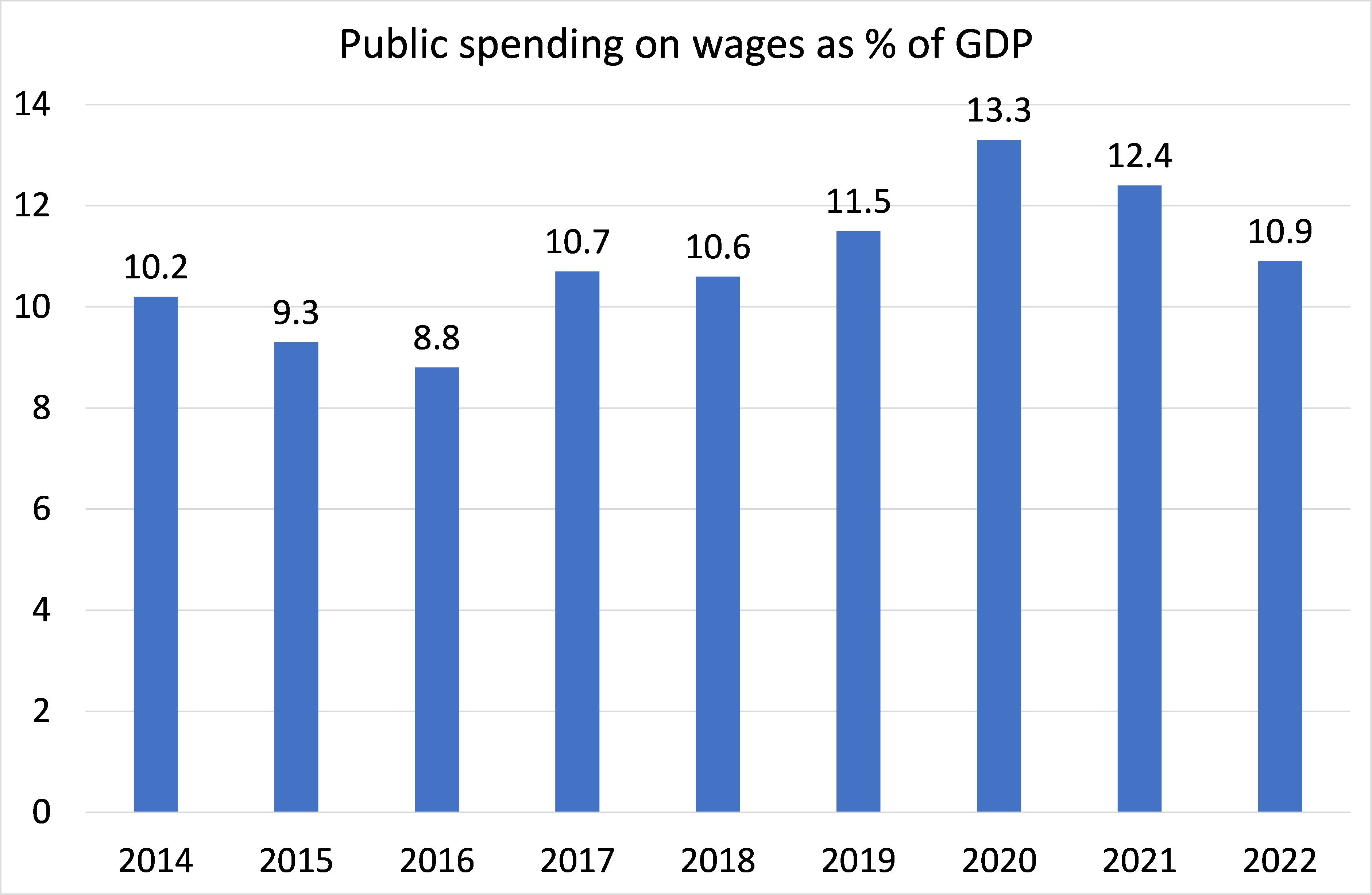

Austerity measures have been applied by various governments over the last ten years. The current IMF package requires a tax increase equivalent to 0.5% of annual GDP, increased pension contributions and rises in energy tariffs. All these measures will lead to a further fall in welfare spending, from 20% of GDP at the time of the 2014 crisis to just 13% this year.

Source: IMF

Source: IMFAt the same time, government must resist any public sector wage rise to compensate for near double-digit inflation rates.

Source: IMF

Source: IMFAbove all, the IMF is insisting, with the support of the latest post-Maidan government, to carry out substantial privatisation of the banks and state enterprises in the interests of ‘efficiency’ and to control ‘corruption’. “The authorities remain committed to downsizing the SOE sector. Adopting an overarching state ownership policy would be a key step. Ultimately, corporatization and the concomitant improvement in performance of non-strategic SOEs should lead to their successful privatization. Preparations are also underway to execute the authorities’ strategy to reduce state ownership in the banking sector. Updated in August 2020, the strategy envisions a reduction in state ownership to below 25 percent of banking sector net assets by 2025.”

Most significant has been the move to privatise land holdings. Ukraine is home to a quarter of the fertile “black earth” soil (Chernozem) on the planet. It is already the world’s biggest producer of sunflower oil and the fourth-biggest producer of corn. Along with soybeans, sunflowers and corn are among the main crops grown in the Sunflower Belt, which stretches from Kharkiv in the east to the Ternopil region in the west.

But agro productivity is low. In 2014 agricultural value added per hectare was $413 in Ukraine compared to $1,142 in Poland, $1,507 in Germany, and $2,444 in France. Land is highly polarized between a small workforce in large mechanized commercial farms and the mass of peasants who farm small plots. About 30% of the population still live in rural areas and farming gives employment to more than 14% of the workforce. One of the great demands of Western advisors to Ukraine in recent years is that it should ‘liberalize’ the land market so that ‘a prosperous growth dynamic’ might be unleashed. The IMF reckons that such liberalisation would add 0.6-1.2% pts to annual GDP growth depending on whether the government permitted both foreign and national land ownership.

The government is resisting allowing foreigners to buy land. But in 2024, Ukrainian legal entities will qualify for transactions involving up to 10,000 hectares and will apply an agricultural area of 42.7 million hectares (103 million acres). That is equivalent to the entire surface area of the state of California, or all of Italy! The World Bank is positively drooling at this opening up of Ukraine’s key industry to capitalist enterprise: “This is without exaggeration a historic event, made possible by the leadership of the President of Ukraine, the will of the parliament and the hard work of the government.” So Ukraine plans to open up its economy even more to capital, particularly foreign capital, in the hope that this will deliver faster growth and prosperity.

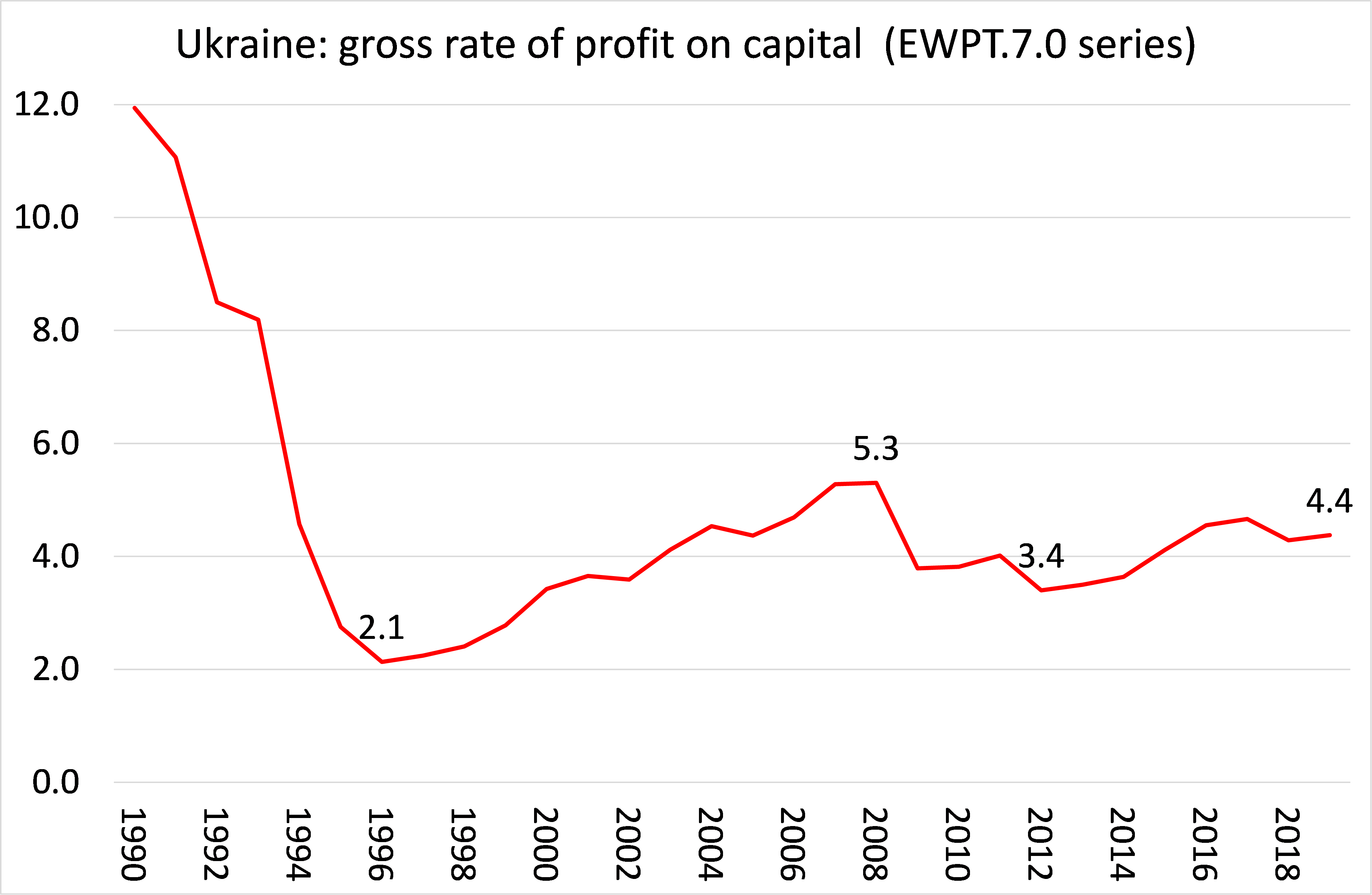

But this is hope only. Current annual economic growth is optimistically forecast to rise to a 4% rate each year while inflation will stay at 8-10% a year. Unemployment remains stubbornly high (10%), while business investment is falling off a cliff (down 40%). That bode well for a capitalist boom. Capital investment is low because the profitability of capital is very low.

EWPT 7.0.series

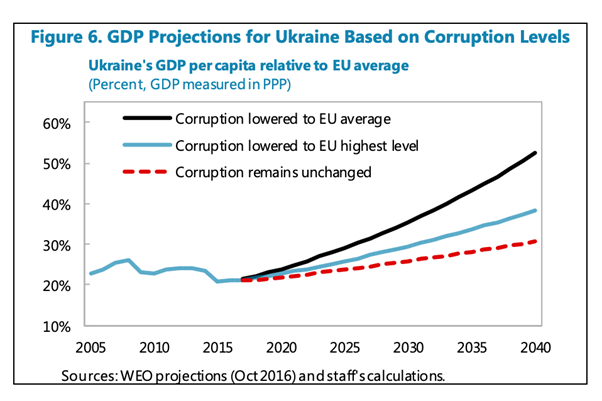

EWPT 7.0.seriesMaybe the riches to be gained from the privatisation of state assets and land will reap rewards for some capitalists, probably mostly foreign investors. But most of the gains will probably disappear as corruption remains rampant. The IMF admits that if corruption is not reduced, there will be no recovery and Ukraine will not catch up with the rest of its neighbours to the West.

Officially, Ukraine’s gini coefficient for income inequality is the lowest in Europe. That’s partly because Ukraine is so poor: there is practically no middle class And the very rich hide their income and wealth, paying little or no taxes. The ‘shadow economy’ is very large, so the top 10% have wealth and income 40 times larger than the poorest Ukrainians. The current World Report on Happiness puts Ukraine at 111 out of 150 countries below many sub-Saharan African countries.

And the conflict with Russia has cost hugely. According to the Center for Economic and Business Research (CEDR), the loss of GDP has been $280bn dollars over six years from 2014 to 2020, or $40bn annually. The Russian annexation of Crimea has resulted in losses of up to $8.3 billion annually for Ukraine, while the ongoing conflict in the Donbas is costing the Ukrainian economy up to $14.6 billion a year. Total losses from these two occupations alone, since 2014, amount to $102 billion. CEBR says the conflict had a significant impact on the Ukrainian economy, including by reducing investor confidence in the country. This, in turn, led to a loss of $72 billion – $10.3 billion annually. The steady decline in exports resulted in total losses for Ukraine of up to $162 billion between 2014 and 2020. The total loss of fixed assets for Ukraine in Crimea and Donbas from the destruction or damage of assets amount to $117 billion. The total amount of foregone tax revenues to the budget of Ukraine for the period from 2014 to 2020 is $48.5 billion.

After the fall of the Soviet Union, and after gaining its official independence in 1994, the people of Ukraine were ravaged by oligarchs who have milked the assets and resources of the country and also by governments swinging their support between Putin’s Russia and the EU. After the Maidan uprising against the rule of the pro-Russian government, ultra nationalists in Ukraine have dominated government policy. They are demanding that Ukraine join the EU and above all join NATO in order to regain the territories annexed by Russia.

The cruel irony is that Germany has no intention of allowing a volatile and very poor Ukraine join the EU – far too much trouble and cost; while even the US will probably baulk at its NATO membership. In turn, Russia has no intention of handing back the Russian-speaking areas to Kiev control and instead is demanding permanent autonomy and an agreement that Ukraine will never join NATO.

The so-called Minsk accords of 2014-5, signed by the major powers and by a previous Ukraine government, cannot reconcile this division. So the Kiev nationalists, encouraged by the US, continue to press and the Russians continue to prepare for a possible invasion to force an agreement to divide the country permanently. Ukraine is trapped between the interests of Western imperialism and Russian crony capitalism.