Chartbook #136: The legacy of Shinzō Abe, yield curve control & the "widow-maker" trade.

The assassination of Shinzō Abe looks to have been the act of a crazed loner. But the circumstances were not merely fortuitous.

When he was shot, Abe was on the stump campaigning on two issues that defined his legacy for contemporary Japan.

Abe was an unabashed nationalist and historical apologist. He is also being celebrated today as the champion of a new realism in East Asian foreign policy. Abe saw Russia’s aggression against Ukraine and mounting Sino-US tension as vindication for his calls for a new Japanese security policy that broke with the postwar taboos. Under the influence of “pivot to Asia”-stalwarts like Kurt Campbell, the Biden administration has re-embraced the alliance with Japan. To many analysts, Abe looks like a prophet of Indo-Pacific containment policy.

On the stump on the day of his death, Abe’s other great talking point was Japan’s economic situation. Here, Abe was on the defensive. His killing comes at a moment when his economic policy legacy is under threat. As the world’s central banks turn to tightening, the question has become ever more pressing whether the Bank of Japan can remain the odd central bank out.

Abe was elected in 2012 with a mandate to adopt an economic policy - soon dubbed Abenomics - based on “three arrows”: flexible fiscal policy, monetary expansion, and structural economic reform.

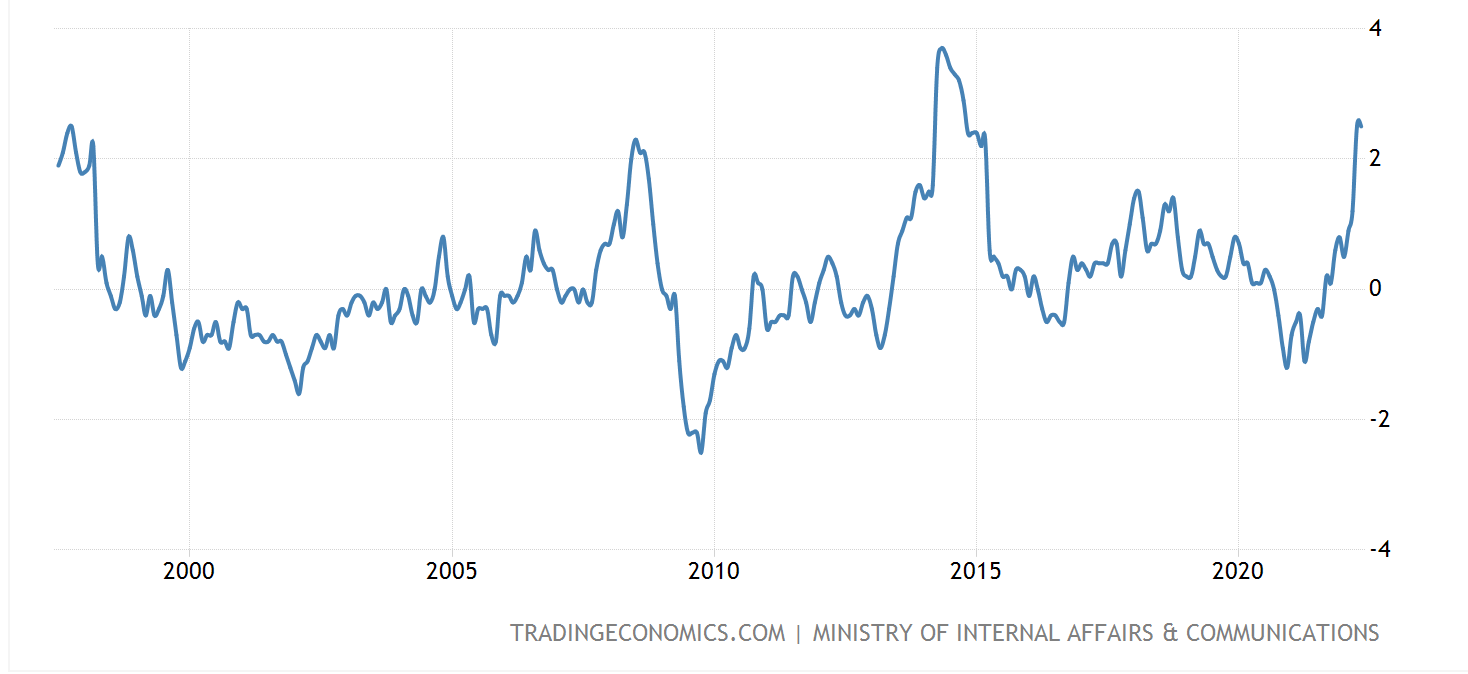

Abe was out of power during the 2008 financial crisis, which hit Japan hard. Compared to the US or Europe, Japan’s banks survived the crisis in relatively good shape, but Japanese exports were dealt a severe blow. This compounded the recessionary and deflationary pressure evident since the 1990s. In the worst months of 2009, Japan recorded an alarming deflation of more than 2 percent.

Japan Inflation

Source: Trading Economics

Falling prices are so dangerous because they form a downward spiral of self-fulfilling recessionary expectations. Falling prices punish those who borrow to fund investment. Abe’s goal was to push Japan above 2 percent inflation and thereby to restore investment and growth.

On the three prongs of Abe’s ambitious agenda, the verdict is mixed.

Abe’s structural reform agenda was a partial success at best.

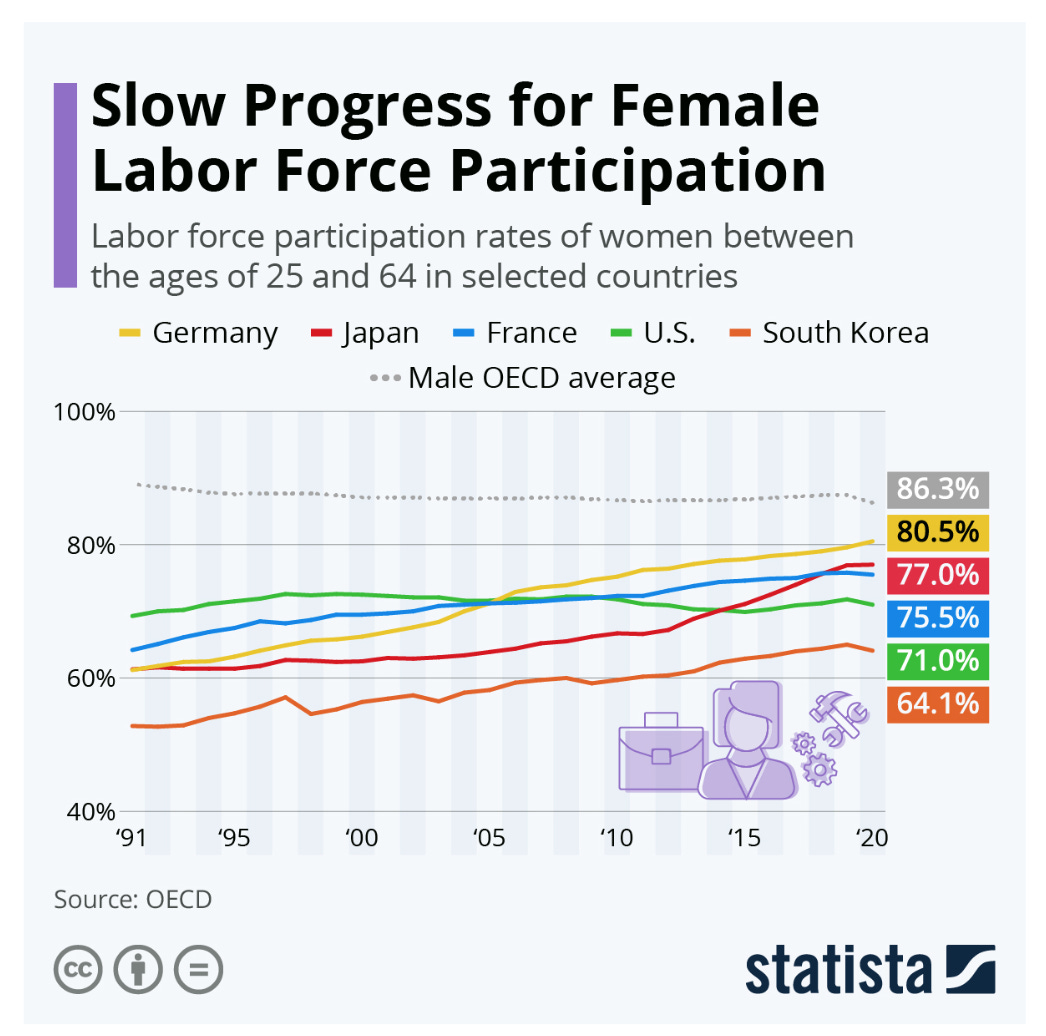

To address Japan’s declining labour force, Abe favored women’s labour market participation. And during his administration Japanese women did enter the labour market as never before. The fact that a significantly larger percentage of Japanese women are in paid employment than in the United States is a remarkable historical turnaround.

In structural terms, however, gender relations were little changed. Japan remained profoundly patriarchal.

Along with Abe’s avowed nationalism, on structural reform his administration presented the picture of an ambiguous experiment in modernization.

By contrast with his agenda of structural change, Abe’s fiscal policy started boldly. In 2013 Abe introduced a stimulus package worth ¥10.3 trillion (equivalent to $116 billion) in government spending. But at the crucial moment in 2014, as the momentum of the early years was stalling, Abe allowed a hike in the consumption tax, legislated by the government of his predecessor, to go ahead.

The retreat from fiscal stimulus left policy walking effectively on one leg. The one side of Japanese economic policy that cannot be accused of half-heartedness is monetary policy.

In February 2013 to flank his expansive agenda, Abe nominated Haruhiko Kuroda to the governorship of the Bank of Japan. He had long been an advocate of looser monetary policy in Japan. Kuroda’s appointment was reinforced by the choice of Kikuo Iwata – another critic of the BoJ’s policies to date – and Hiroshi Nakaso, a senior BOJ official in charge of international affairs, as his deputies.

Kuroda and his team immediately adopted a policy of aggressive monetary stimulus, doubling down in 2014. When this was not enough in January 2016 the BoJ resorted to a policy of negative interest rates followed in September 2016 by the adoption of yield-curve control, centered on the Japanese 10 year bond. The Bank of Japan effectively committed to buying bonds in sufficient quantity to ensure that 10-year JGB yield remains around 0 percent and deposit rates remain at -0.1 percent .

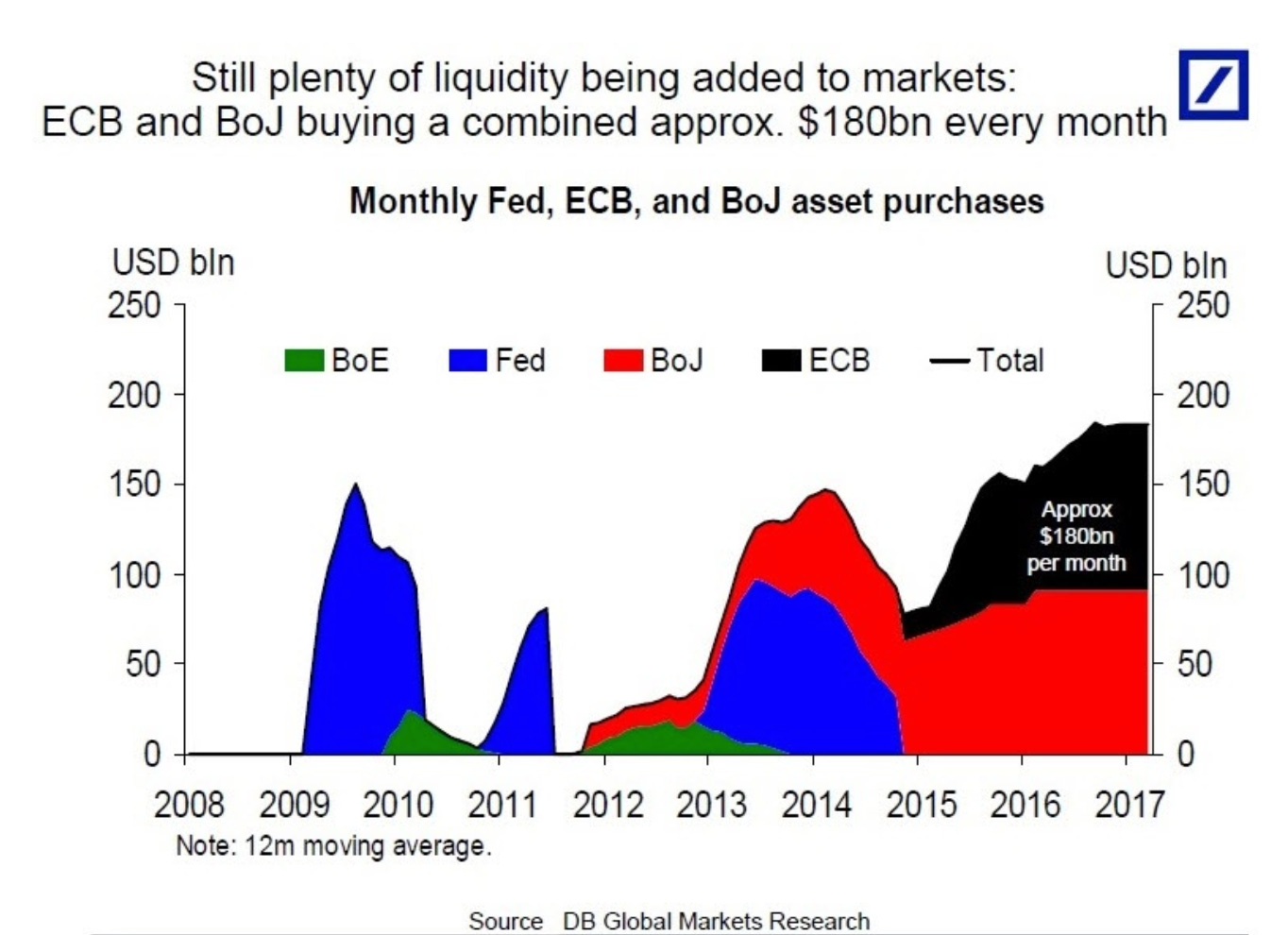

The 2016 shift was driven by domestic factors but also by global forces. 2015 was an extremely nervous year for the world economy. China suffered a major sell-off in stock markets and the economic growth miracle wobbled. Europe’s situation prompted EU Commission President Jean-Claude Juncker to first use the term poly-crisis. Ukraine, the Syrian refugee crisis, Greece’s debt crisis all came together. The ECB feared the worst. Inflationary expectations were slumping into deflationary territory. Would the Eurozone under the weight of inadequate investment and too much austerity slump into Japanese territory? In March 2015 the ECB responded by launching QE on an unprecedented scale.Previously, the ECB had bought bonds only to stabilize specific markets. Now it did so wholesale.

The Fed may be the undisputed leader amongst global central banks and Ben Bernanke led the charge in 2008. But, together, the scale of the ECB and the BoJ’s program bond buying after 2015 dwarfed anything the US had previously attempted.

This convergence of policy between Japan and Europe was not simply a matter of politics. Both Japan and Europe were suffering from chronic surpluses of savings, above all in the corporate sectors. The former champions of industrialization and export-driven growth were no longer investing enough at home. Sustained public investment i.e. fiscal policy, was the advice given by most economic experts. But given the obstacles to that in both Japan and Europe, central bank policy was the “only game in town”.

In 2015-6, the world avoided recession, but it was now profoundly imbalanced. The Fed under Janet Yellen was tightening. The ECB and BoJ were fully expansionary. The result was that the euro and the yen depreciated against the dollar, triggering a mini-recession in US manufacturing in 2016. Tough times in the rustbelt helped to set the stage for the victory of Donald Trump in November 2016, a nationalist populist with whom Shinzō Abe got along far better than most other world leaders.

In his effort to Make America Great Again, Trump adopted his own version of Abenomics, focusing on big tax cuts. Initially, this put him at odds with America’s central bank. The Fed first under Yellen and then Jerome Powell continued to attempt to “normalize” policy. In 2019 this produced mounting political and financial market tension in the US with former Fed officials openly taking positions against the Trump administration. After some months of jitters, culminating in the nasty incident in the US repo market in September 2019, it was the Fed that gave way. Jerome Powell abandoned his effort at tightening monetary policy. Mario Draghi, in his final months in office in Frankfurt, did the same. The ECB resumed bond buying.

As 2020 began, before news of COVID spread, it seemed that the Japanese model had won. More than a decade on from 2008, there was no alternative to continuing unorthodox monetary policy. The shock of COVID only reinforced this impression. Every central bank did it differently, but everyone intervened and did so on a massive scale. In Japan, to counter COVID, Abe’s administration adopted a giant fiscal and monetary stimulus - rated at 20 percent of GDP.

As Abe was force out of office by ill-health in September 2020, it seemed that at least as far as monetary policy was concerned the whole world had “gone Japanese”.

In 2020 the RBA in Australia adopted yield curve control in explicit imitation of the Bank of Japan, with whose economy Australia is closely connected. The ECB was not targeting the yield curve but it was hard to deny that it had an eye on spreads, which are the yields that matter as far as the eurozone is concerned. In 2021, both the ECB and Fed adjusted their policy framework for a world in which the Japanese problem of secular stagnation and ultra-low inflation was assumed to be the backdrop.

And then the poly-crisis took another unexpected turn. Rather than stagnating, first the price of energy, then commodities and then the price of many other things began to surge. Even in Japan, inflation ticked up. In Europe and the US the shock was dramatic.

This faced the central banks and bond markets with an unexpected dilemma. It was clear that central banks would have to reposition themselves. And by the autumn of 2021 this was causing deep anxiety in global bond markets.

As bonds sold off hard, promises to prop up prices and keep yields down lacked credibility. In November 2021 as markets became disorderly the Reserve Bank of Australia was forced to abandon its version of the the Japanese policy of yield curve control. The RBA was no longer willing to muster the fire power necessary to peg rates. Yields surged out of control.

Australia is a relatively small player. Though the RBA’s about-face added to uncertainty, it did not destabilize global markets. It was indicative, however, of a broader shift. Many emerging market central banks around the world, led by Brazil, were already raising rates. By early 2022, both the Fed and the ECB were clearly indicating the end of QE and the move to tightening. This has left the Bank of Japan isolated.

Fumio Kishida, as Abe’s successor, had promised to honor the legacy of his predecessor’s economic policies. And in November 2021 he made good on that promise with a giant fiscal stimulus. Meanwhile, at the BoJ there is continuity of leadership and commitment. On the day of Abe’s assassination, his monetary policy legacy remains intact. But the question is how long this can continue.

With other central banks raising interest rates around the world, to peg Japanese rates at low levels, the BoJ has had to buy bonds at a dramatically accelerated rate. Even by the standards of its long history of experimentation, the current policy stance is extreme.

As the FT reports, global investors are increasingly betting that this cannot continue. They are positioning themselves to take advantage of a BoJ move to follow Australia and release yields. If you short Japanese bonds, you may be in a position to take advantage of a Bank of Japan exit from the market, falling bond prices and rising yields.

This is not a new trade. Indeed, it has been attempted so many times without success that it is known in the financial markets as the “widow-maker”. But might this time be the moment in history when the Bank of Japan reverses direction? Pressure is clearly building.

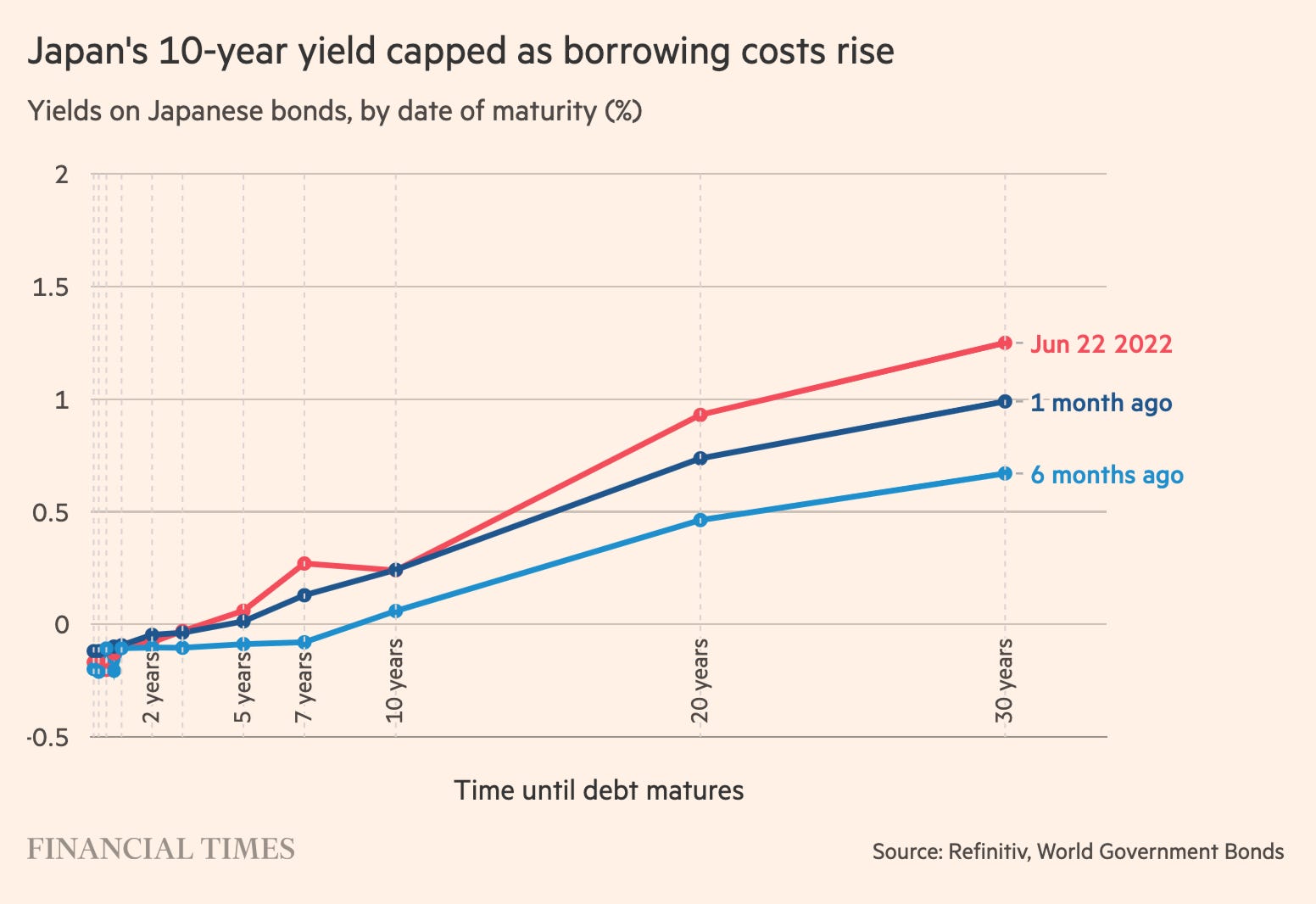

Aside from the 10-year yield, which is pinned by the BoJ’s policy, shorter and longer-term borrowing costs have been pulled upwards as global interest rates rise. Japan’s yield curve — the graph of its yields across increasing maturities — would usually be a smooth upward-sloping line. But it has developed a distinct kink around the 10-year point.

The uncapped yields on 7-year debt, are now above those on 10-year, which the Bank of Japan is targeting. This gives a clear indication of how the curve would adjust if the Bank of Japan removed its support.

Domestic Japanese investors continue to maintain faith in the Abe-Kuroda formula. Too much political capital has been invested over the last decade in the BoJ’s adventurous program. Publicly, the BoJ too remains completely committed to its stance.

At last week’s policy meeting, the Japanese central bank renewed its pledge to buy as much government debt as it takes to keep 10-year borrowing costs below 0.25 per cent.

The Bank of Japan has more than reputation invested in the continuity of policy. If it loses control of yields and bond prices plunge it could face a paper loss of as much as $200 billion on its huge bond portfolio.

There is determination, therefore, to continue. On the other hand, those shorting the trade insist that this veneer of continuity cannot be taken at face value. If the BoJ is to have any chance of managing the exit from its strategy in an orderly way, it must remain in charge of the narrative. That means that it must give no advanced warning to the markets of a potential change in position. The change must come as a complete surprise.

If the Bank of Japan maintains its policy, on the other hand, the pressure will show up not only in the bond markets. The Japanese currency is really feeling the pressure of continuous monetary expansion and low interest rates.

In a period of dollar strength, the yen has devalued dramatically against the US currency, falling to a 24-year low. This adds to the competitiveness of exports and raises the cost of imports, which helps to counter any deflationary tendency. But the sheer speed of the devaluation also spreads uncertainty to Japanese investors. Would they be better off investing abroad? How long can the devaluation continue for?

Compared to this scenario of mounting pressure in bond markets and a serious devaluation, many think the Bank of Japan would be better advised to bite the bullet and initiate a policy shift. After all, it is in a position, somewhat unexpectedly, to declare victory. Inflation in Japan has for the first time since 2015, exceeded the level of 2 percent that Abe’s government initially set as its objective.

If the Bank of Japan does decide to change direction, how it does so will be crucial. Australia’s exit from yield curve control, was, as the Bank’s own analysis now admits, a bit of a shambles. The Bank of Japan unlike the Reserve Bank of Australis is a whale. If it attempts an exit from unconventional policy and it goes wrong, it could send shockwaves through bond markets worldwide. It might also imperil the forward momentum of the Japanese economy. In any case, it would be the end of an era that will, forever, be associated with Shinzō Abe.