BIG by Matt Stoller

Welcome to BIG, a newsletter on the politics of monopoly power. If you’re already signed up, great! If you’d like to sign up and receive issues over email, you can do so here.

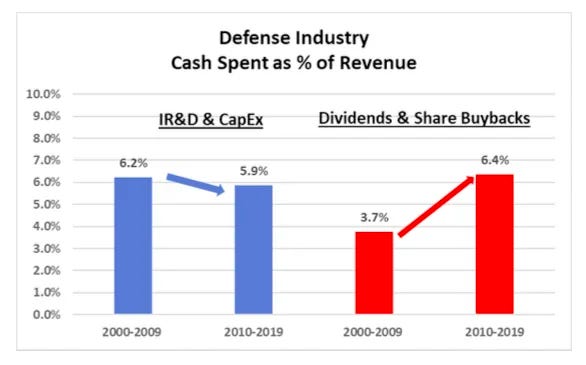

Today I’m writing about an astonishing report that came from the Pentagon this week on how Wall Street has wrecked the defense industrial base. This chart, which shows stock buybacks are up while research and development is down, is the key finding.

“Despite

improving profit margins and cash generation for defense contractors in

2010-2019 vs 2000-2009, the share of contractor spending on Independent

Research and Development (IR&D) and capital expenditures declined

while cash paid to shareholders in dividends and share repurchases increased by 73%” - DOD Contract Finance Study Report, April 2023

Before I get to that, I have a few announcements. First, there’s some good BIG-related news. Montana Congressman Ryan Zinke is demanding an investigation into Booz Allen’s Recreation.gov contract and the consulting giant’s control over national parks. As you may recall, I broke the story about Recreation.gov late last year, and the Wall Street Journal did a follow-up on it last week. There’s also a class action complaint against Booz Allen. So yay.

Second, I’ll now be sending occasional shorter missives to paid subscribers. On Wednesday, I sent out a shorter quick read on how Wall Street expects action against drug middlemen. Don’t worry, I’ll still be writing the longer stuff. If you want access to all the writing and the BIG Discord server, you can subscribe here.

And now…

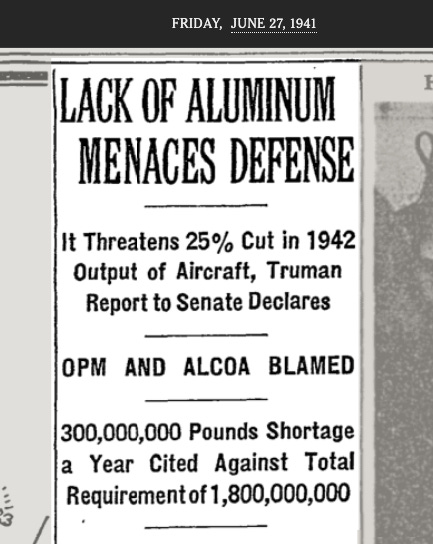

On the eve of Germany’s invasion of Poland in 1939, America was woefully unprepared for a conflict that everyone thought would come. Most strategists knew the nation that could produce more with its industrial base would probably win, and yet even so, the American business world was oblivious. 85% of U.S. factory machinery dated from the 1920s or earlier, and some predated the Civil War.

And the deeper one looked the worse the situation seemed. The next war would be fought at the cutting edge of technology, which is to say, with airplanes. And an air force required the technological marvel of aluminum, which you could only get from the longest-lasting industrial monopoly in U.S. history, the Aluminum Company of America, or Alcoa. Aluminum, light and strong, was also immensely energy-intensive to create, and Alcoa organized production of 100% of it.

The President of Alcoa, Arthur Davis, a hoarder of talent, tools, and inputs like bauxite, wasn’t worried. He had promised there would be no shortage, that Alcoa, modern and sophisticated as it was, could fulfill all military and civilian demand, and then some. Yet even before the entry of America into the war, Davis was proven wrong. Aerospace firms just couldn’t get their hands on enough of the wonder metal.

After America joined the fight, the shortage got worse. “Prime Minister Churchill said of the Royal Air Force that never in history did so many owe so much to so few,” wrote investigative journalist I. F. Stone. “It might be said of us that never did a people do so little with so much,” he added. Politicians were furious at Alcoa, as were military leaders. FDR demanded 50,000 airplanes a year, and the U.S. delivered that, and more. But to do so, the national security apparatus, which has always lurked in the background of monopoly power questions, had to help break Alcoa’s power, through a mammoth antitrust suit, as well as industrial strategy in the form of subsidies to nascent rivals.

Today, we face something similar. Not a world war, fortunately, but a collapsing defense industrial base that limits the American ability to supply its military. And increasingly, American leaders are angry, not at Alcoa this time, but at the defense contractors who hold market power over what the military buys. From Javelins to ordinary ammunition to ship repair to ball bearings, the U.S. military just can’t get what it needs. “I am not forgiving of the fact that you’re not delivering the ordinance we need,” said Admiral Daryl Caudle at Surface Navy Association conference earlier this year. “All this stuff about COVID this, parts, supply chain this, I just don’t really care. We’ve all got tough jobs.”

I’ve been writing about the defense industrial base monopoly problem for years at this point; the first major piece I did was in the American Conservative in 2019. The modern story is relatively simple. In the 1990s post-Cold War era, the White House sought to cut defense spending. Bill Clinton’s administration arranged a deal with defense contractors; they would tolerate lower revenue or stagnant revenue, if they got higher margins. And so at a dinner known as ‘The Last Supper’ held in the Pentagon, the Clinton Defense Department encouraged a merger wave. Throughout the 1990s, the DOD even paid the merger costs of its defense base firms; the number of major prime contractors (or ‘primes’) dropped from dozens to 5. In addition, Congress, under ‘Reinventing Government,’ passed laws to eliminate contracting rules that blocked price gouging of the treasury.

All of this monopolization was done in a unipolar moment, when just-in-time manufacturing where suppliers kept no inventory on hand was applied to everything, even military stockpiles. This was, in retrospect, insane. Who thinks that having no resiliency is a good strategy for wars? And yet, the U.S. felt so confident in its geopolitical position that the Clinton administration even helped China build its missile program - aimed at the U.S. - with U.S. technology, all to do a favor for the McDonnell Douglas corporation. The military defense base continued to fall apart, for decades, throughout the Bush, Obama, and Trump administrations.

So that’s the bad news.

The good news is that some of our leaders have finally started to wake up to this strategic problem. Somewhere between 2019 and 2022, military thinkers began to understand that we are in trouble. The realization that China has a military that could potentially defeat the U.S. prompted significant concern. China’s ability to build things is a big reason why. “In purchasing power parity, [China] spends about one dollar to our 20 dollars to get to the same capability,” said Maj. Gen. Cameron Holt from the US Air Force acquisition, technology, and logistics office.

Then in 2020, factories in Mexico that make defense base materials as part of the just-in-time model of supply chain management closed down, against the Pentagon’s wishes. In 2022, the Ukraine war, which depleted U.S. military stockpiles, accelerated a conversation over geopolitics, with leaders on the right like Elbridge Colby forcing a conversation over trade-offs between China, Russia, and the Middle East. On the left, Democratic anti-monopoly leaders like Elizabeth Warren, Ro Khanna, and John Garamendi saw the problem as well.

Since Covid and increasingly during the Ukraine conflict, policymakers have realized the U.S. faces real physical constraints on what we can build. Consider that the U.S. still cannot replenish its stocks of Javelin and Stinger missiles. Why? Not because the money isn’t there, but because if defense contractors act too quickly, they would, as one consultant to the industry put it, “get hammered by Wall Street.” And since there’s virtually no competition at this point in building any weapon major system, there’s no rush to take market share.

Today, leaders in and around the Pentagon are starting to act to remedy the situation. Kathleen Hicks, who is the number two at the Defense Department, helped block a merger of Lockheed and Aerojet, and that successful challenge ended a merger spree in the defense industrial base. The problem isn’t fixed. But we’re getting closer.

And that brings me to the Pentagon defense finance contracting report that just came out on Wednesday, which was the first wholesale reexamination of the “effect that the DOD’s contract financing and profit policies have on the defense industry” since 1985. Most DOD reports are meek, but this one attempted wholesale change in the framing of the relationship between contractors and the Pentagon. After reading it, I have to say someone in the bureaucracy is very angry at Lockheed Martin, Boeing, Raytheon, Northrop Grumman, and General Dynamics.

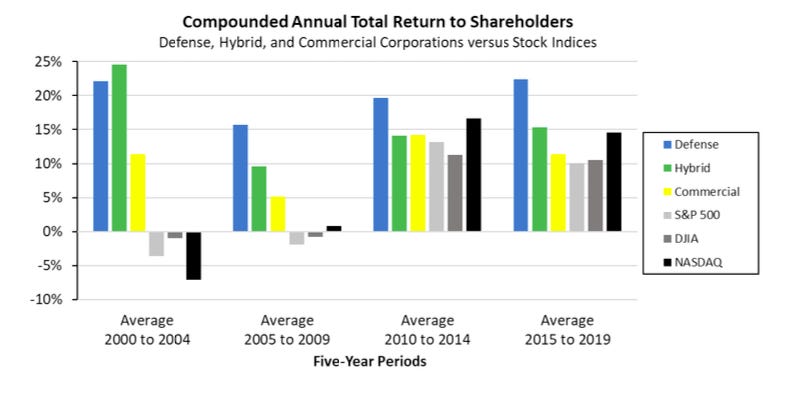

The DOD tasked three universities with examining how Pentagon contracting works, and did an internal analysis, all to determine the financial health of the defense base. And what they found is not so different than health care, big tech, finance, or any other industry segment; defense is run by a few giant middlemen who do exceptionally well by shareholders, outperforming commercial rivals and the S&P index. Contracting doesn’t look especially profitable, but the relatively lower margins are more than compensated by a host of favorable contracting terms offered by the government.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. This is journalism and advocacy that challenges power, so please consider a paid subscription. You can always get lies for free. The truth costs a few bucks, but in the long run it’s much cheaper.

Of course, like middlemen in other industries, the big guys don’t really produce, they extract. The actual work, 60% to 70% of it, is performed by subcontractors, and these firms have very few rights and get paid when the big guys feel like it. The executives at Lockheed Martin or Raytheon, in other words, act a lot more like financial engineers than actual engineers.

The net effect is the following: “Despite improving profit margins and cash generation for defense contractors in 2010-2019 vs 2000-2009, the share of contractor spending on Independent Research and Development (IR&D) and capital expenditures declined while cash paid to shareholders in dividends and share repurchases increased by 73%.”

And there are charts!

Ok, let’s go to the details. First, the report argues that being a prime contractor is a very good business to be in. Defense primes are financed by the government, paid promptly, and bear very little financial risk for anything they do, including research and development, or building and sustaining capital assets like machinery and dry docks. Here’s an accompanying chart to the report, comparing the defense work to normal commercial work.

Cash flow in the defense industry is thick and predictable. Profit margins are lower in defense, but the “gap is more than offset” because defense firms don’t have to invest very much, since their working capital is mostly provided by the government. Indeed, most of the business of being a big defense contractor seems to come down to cash management, or what Brandeis called subsisting on 'other people’s money’, in this case, that of the taxpayers.

“Defense companies have higher total returns to shareholders compared to their commercial analogs, or when compared to broad equity market indices such as the S&P 500.”

Here’s how it works. Defense contracts for non-commercial items often appear to be relatively low margin arrangements, with a small mark-up on a unique defense item. The cost of building an item might be $100, and so a contractor will build it and get paid the cost plus, say, $10, for a 10% profit margin. That’s good, but not great. So why are defense stocks such good investments? The reason is because contractors don’t have to use their own cash to pay for anything. If I’m using $10 of my own money, and $90 of the government’s money to build a widget, and I get a $10 profit from selling that widget, it might look like a 10% profit margin. But the internal rate of return on the cash that I’ve put down is $10 generated by putting down $10, or 100%.

That’s not only a great return, but in the defense space, it’s all risk-free. Any cost overruns, or needed research, can be billed to the government, plus the usual mark-up. If the government kills the contract, or changes requirements, no worries. If labor charges go up, so do contractor profits. Even depreciation, which is to say a factory becoming less valuable over time because of wear and tear, gets reimbursed almost immediately with cash. (And the immediate reimbursement rate went up during Covid, from 80% to 90%, to improve contractor cash flow.) It’s astonishingly cushy. In other words, the trick for primes is to have very little of their own working capital involved, yet still to get returns on all the government money they spend.

So far, I’ve just explained why it’s an easy business model, though not a destructive one. The government might overpay a contractor, but at least it gets Stingers and Javelins. Here’s the problem. Though the primes get risk-free returns off of other people’s money, the subcontractors who do the actual work get nothing of the sort. In 2022, over a quarter of subcontracting invoices were paid late, and this rose to 33.2% for small business invoices. Subcontractors usually don’t know who the contracting officer in government is, so they can’t complain. Often smaller firms don’t even know they are making products that will be sold to the government.

It gets even worse. From 1971-2000, there was a “paid cost rule” for large primes, where contractors had to have paid supplier invoices before billing the government. In 2000, that rule was eliminated, which allows “contractors to be paid by the Government before they pay the supplier.” Now that’s a great business model, to order work from someone else, bill the government for it, get paid, hold the cash for awhile, and then pay the supplier late. The failure to provide cash to the subcontractors that actually make stuff might be one reason it’s so hard to ramp up production.

“When industry has generated additional profits and cash, what has it chosen to do with it? The data in this study points to one answer: Industry did not choose to spend it on IR&D and CapEx. It chose instead to significantly increase the percentage of cash paid to shareholders in the form of cash dividends and share repurchases, thereby reducing the amount of invested capital for the corporation.”

There’s also what the government gets for its money, notably, who gets to the keep the intellectual property rights when firms invent stuff.

When IR&D efforts do result in a technological advance, despite the fact the Government paid the cost of the IR&D (plus profit), current laws and regulations allow the contractor to own the intellectual property (IP) rights to anything developed with IR&D funds. When this occurs, and the contractor receives the IP rights, it only strengthens the contractor’s position as a sole-source contractor for a product and can lessen the likelihood of facing competition for sustainment efforts for that product in the future.

As Marine officer Elle Ekman wrote years ago in the New York Times, a lot of soldiers are not even allowed repair their own equipment because of these IP protections, even though the government paid to develop the technology. Keep in mind, while this stuff is gross and corrupt, it’s the Pentagon itself, through its internal evaluations, exposing it. So it’s *good news* that it’s being talked about, and shows that some officers at DOD want it fixed.

The last part of the report worth noting is a vicious, if passive aggressive, attack on the lobbying efforts of the primes. The report highlights a couple of dishonest claims.

First, contractors say that it is so very very hard to be a defense contractor.

One defense industry association characterized the health of the the defense industrial base as being “fair to poor;” another described it as “at risk;” and another cited a 2022 defense industry association report which gave it a “failing grade.”

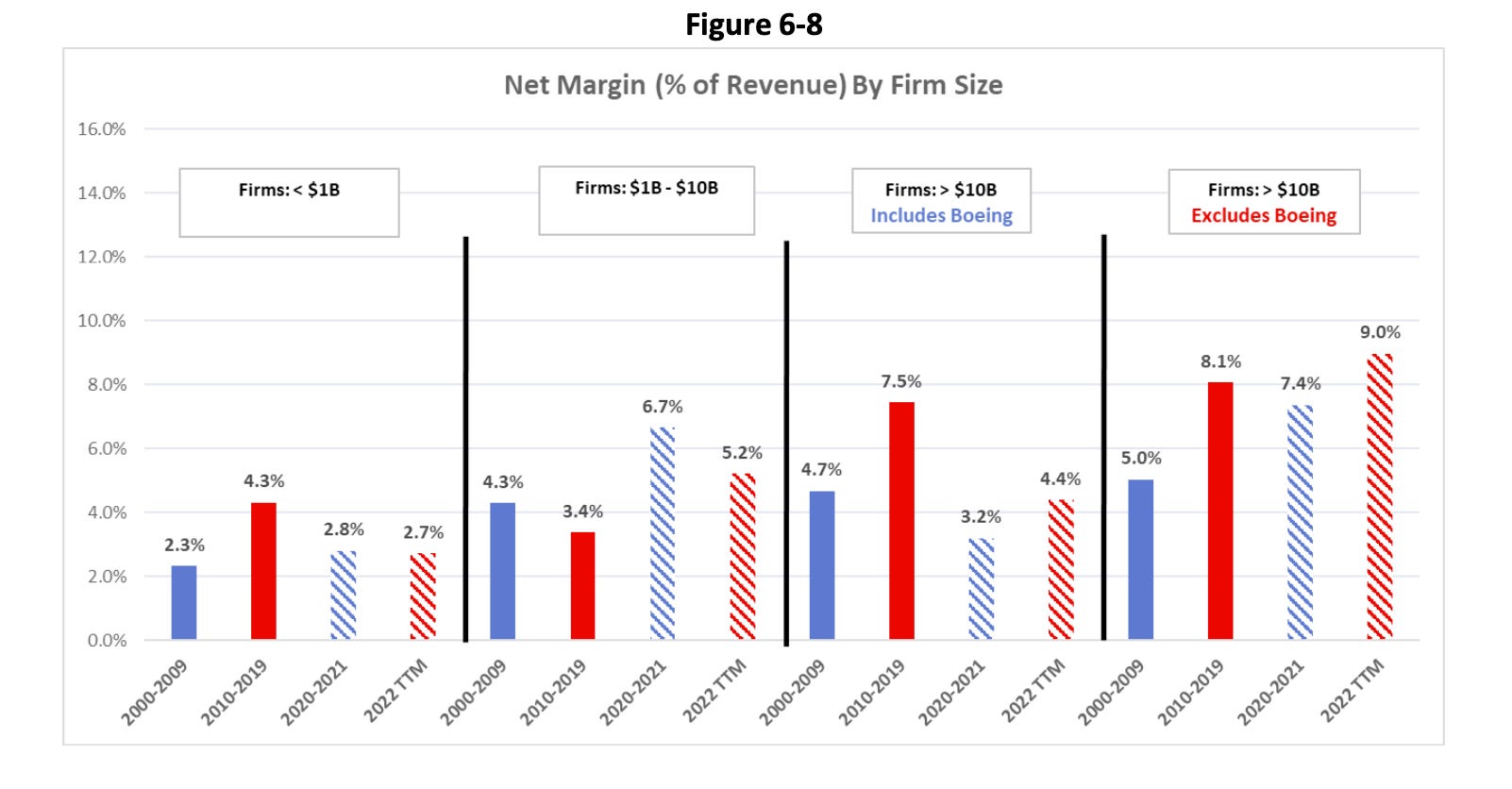

Is that true? No. “These industry association comments regarding the health of the Defense Industrial Base (DIB),” wrote the report, “are difficult to reconcile with defense industry financial data.” And then the report pointed to this chart.

Second, the report disputes the claims by defense lobbyists that the instability of the Federal budgeting process hurts their profits. You know how bad Congress is, yada yada.

Two defense industry association commenters identified DoD budget instability and Continuing Resolutions which averaged 129 days for 2000-2009 but 177 days for 2010-2019, sequestration which began in April 2013 and ended in 2021 and the decreased use of performance-based payments which, per one defense industry association, dropped from 76% in 2010 to 36% in 2016.

Is that true? Also, no. “Based on these industry comments,” the report said, “financial performance should have degraded in the 2010-2019 timeframe but the financial statements for defense contractors showed a significant improvement over the prior ten years (2000-2009).”

Third, the report disputes the industry rationale for all the cash flow the government is providing, which lobbyists argue is critical for research.

Defense industry association commenters specifically cited the importance of using cash to invest in research and development and capital assets. In its comments regarding capital investments, one defense industry association specifically stated: “In most cases the profitability for government customers is insufficient to finance the investments.”

And this one? Once again, no. “This assertion did not appear to be demonstrated by the data,” it said. And then the authors specifically called out Lockheed Martin for misleading investors on that point:

IR&D (independent research and development) in the defense industry is often inaccurately referred to as an “investment” a contractor makes on behalf of the warfighter. This study reveals that the opposite is true. IR&D is an investment by DoD and IR&D is a generator of revenue, profit and cash flow for the contractor…

For example, in Lockheed Martin’s 2019 annual report it makes two statements regarding “company-funded” R&D. The first statement appears early in its annual report on Page 16 and indicates that company-funded means “using our own funds” while the clarifying statement referenced in Note 1 appears 51 pages later and indicates that “company-funded” costs are “generally recoverable on customer contracts with the U.S. Government”.

Fourth, the report shows that excuses over Covid and inflation are just that. The report cited one defense trade association claiming that supply disruptions due to the pandemic and inflation were financially devastating. Here’s the cited comment:

For example, the COVID-19 pandemic impacted industries across the entire economic spectrum and did not spare the Defense Sector. This is particularly true for companies that maintain both defense and commercial applications. These companies, due to the pandemic and the subsequent widespread shutdown of the economy, saw their margins eviscerated and internal business planning severely disrupted. This extended across the supply chain, as both large and small companies experienced disruptions, delays, and other hindrances that ultimately had serious ramifications on financial health.

Yet, while the pandemic continues to evolve and impact society in new ways, a new issue has developed which is proving increasingly devastating: Inflation. Historically, inflation has existed at a level between 2-2.5%, allowing for a certain degree of stability when budget planning. However, as this economic indicator has risen dramatically over the preceding year, entities across the DIB have felt the effects of rising prices.

Once again, not true. “The data,” wrote the report, “did not support the implication that COVID-19 had serious ramifications on financial health across the defense supply chain.” Here is one accompanying chart, which separated out Boeing because of its size and unusually large financial hit from Covid.

It’s hard to convey just how much dishonesty from the industry the report authors helped disabuse. They pointed out that arguments characterizing as onerous certain accounting methods known as “cost accounting standards” for contractors, and claiming these requirements kept non-defense firms from contracts, were silly. These requirements “impact less than one eighth of prime contractors,” and usually only the biggest ones who have monopoly, aka sole source, contracts.

The report made a number of recommendations, mostly focused on making sure subcontractors get paid more promptly, and that the government provide cash for primes based on whether they are doing quality work. Restoring the paid cost rule, or letting subcontractors know they are making something for the government and who they can complain to, would be useful as well. But more broadly, it’s clear that it’s time for a rethink of the defense base, if internal R&D is declining despite it being a reimbursable expense and profit center.

What’s fascinating about this report is that it doesn’t even touch some of the main bad contracting practices, which involve characterizing products sold to the Pentagon as ‘commercial items’ and thus exempt from most requirements. But touching as it does just a part of the problem shows why production of military supplies is so expensive and slow. I don’t know how much this report will penetrate the DOD’s actual practices. For instance, Boeing is telling the Pentagon it can speed up deliveries to Ukraine if the DOD waves contracting rules. So we’ll see.

Ultimately, breaking up the big primes is the best route to reform, since that would make it faster for dollars spent to turn into products. Because as it turns out, the reason that dumping lots of cash into prime contractors doesn’t result in what the armed forces need is because prime contractors are cash management machines who occasionally delegate grubby work to subcontractors dependent on them. Executives at the primes do not want to build weapons or military material for the Pentagon. They prefer managing the easiest risk free money generating machine in history. And because of the rules that let them grab cash flow regardless of industrial output, they often don’t need to produce a single functioning thing.

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller