China is Just Fine Thank You!

What amounts to widespread “concern trolling” and misinformation by the Western media, state and social commentators about China is more a projection of their wishes for a weaker China rather than any reflection of reality. Let’s review some of the widespread and obviously coordinated tropes that are being spread by the so concentrated Western media, the paid propagandists of the state and the “sell my soul to the highest bidder” careerist social commentators.

“Slow” Chinese growth

“Low” Chinese domestic retail demand

“Huge” Chinese trade surplus

“Housing Crash” threatening a financial disaster

“Deflation” threatening a financial disaster

“Autocratic” state unable to compete with the flexible “democracies”

“Demographic Time Bomb”

Progress but “At What Cost”

“Slow” Chinese growth

Here is Chinese GDP growth for the past few years:

2020: 2.24% (US was -2.2%)

2021: 8.45% (US was 6.1%)

2022: 2.95% (US was 2.5%)

2023: 5.25% (US was 2.89%)

2024: 5% (US was 2.8%)

2025: forecast to be around 5% (US forecast to be 1.5% to 1.8%)

Cumulative: China 32.5%, US 14.5%. Between 2020 and 2025, the Chinese population actually shrank a tiny bit so all of that growth turned into GDP per capita growth. While the US population officially (i.e. not including illegal immigrants) grew by 3.2%. So, Chinese GDP per capita increased slightly more than 32.5% during these years, while US GDP per capita increased by 11% (1.145/1.032); that’s three times faster in China. If China maintains its “slow” 5% growth rate while its population slowly declines, Chinese GDP per capita and the size of its economy will double every 12.5 years!

“Low” Chinese domestic consumption

In May 2025, retail sales increased 6.4% year on year; about what would be expected with the growth in GDP per capita plus a little bit of inflation. But Western economists and commentators keep complaining that Chinese consumption levels are only half that of Mexico and only one third the level of Japan! I have already noted a number of times that using comparisons based upon market exchange rates can utterly misrepresent relative levels of GDP, GDP per capita and consumption.

That is why there is something called purchasing power parity (PPP). But as Zichen Wang points out, the official PPP numbers calculated by such bodies as the World Bank and IMF may also be highly inaccurate. To investigate this, the China Finance 40 Forum (CF40), which is a leading Chinese independent think tank, decided to carry out a quite extensive review of Chinese consumption levels using actual volumes of consumption, bypassing the issues of relative prices. As an aside, CF40 publishes quite a bit of interesting research in English, here.

And their resultant report found that even the official PPP figures were way off. It stated that:

China’s consumption levels are systematically underestimated

This primarily stems from price advantages and exchange rate deviation

There does remain considerable room for further expansion

Some rebalancing between domestic consumption and external trade would be possible

The gap between the developed nations (including the US, Germany, Japan, France and Mexico) and China across various consumption sectors is much less when measured by actual consumption volumes rather than by per capita consumption expenditure. That’s because the Chinese get more for their money, with an excellent example being the very low prices for good quality cars in China with respect to Western nations.

When it comes to food consumption, China has surpassed the levels of developed countries. The consumption of manufactured goods is on par with countries at the same stage of development. Consumption of healthcare and education services is on a par with developed nations, while there is a small gap in tourism. Instead of being half the level of Mexico, China’s consumption levels are in fact higher than Mexico’s. And at least half the levels seen in countries such as Japan, Germany and France.

In my own analysis of Chinese relative consumption levels I found that, taking into account the US statistical over-estimations (e.g. systematically misrepresenting inflation as being lower than it really is, over-estimating value added in such areas as healthcare, usage of implied amounts, counting rentier costs as value added activities), Chinese consumption levels were about two thirds the level of those in the US. Such a reality would cause a severe cognitive shock to the average American citizen, and cause them to question the legitimacy of American “free market democracy”. Exactly why the US state, oligarch-owned media, and bought and paid for influencers spend so much time attempting to show that the Chinese are still poor and their consumption is being kept low by the “autocratic” and “anti-democratic” Party-state.

Another bug bear that we must also deal with is the whole “China was as poor as sub-Saharan Africa in 1979” just before Deng’s reforms. No it bloody well wasn’t, China was far more developed than sub-Saharan Africa due to the three decades of huge progress made since the 1949 revolution. The years of Mao’s leadership were a great success for China, and provided the very strong and developed base from which Deng could launch his liberalizations. Deng was also helped massively of course by the lifting of the brutal economic and technology blockade upon China by the West, and did not need to redirect large amounts of resources to save the North Koreans and Vietnamese from Western aggression.

China does have some room to increase consumption, to offset any drop in export demand, but the Party-state also understands that the growth of the productive forces should precede the growth in consumption for sustainable long-term growth. The exact opposite of the assumptions of Western economists, politicians and commentators as the West has become much more indebted while the productive forces have waned.

“Excessive” Chinese trade surplus

China’s trade surplus in 2024 was 5.6% of GDP in 2024, rising from 4.6% in 2023, 2.6% in 2021, 1% in 2019, and 0.66% in 2018. In 2018, Germany’s trade surplus was 6.8% of GDP , in 2019 7.25%, 2020 7%, and in the post pandemic period 4.16% in 2023 and 5.7% in 2024. The greatest culprit of “excessive” trade surpluses is a Germany that has maintained such surpluses for two decades (in 2010 it was 5.75% of GDP, in 2005, 5.2%). So why have we not constantly been hearing about Germany “excessive” trade surpluses that must be dealt with for the past two decades?

As we can see from the above data, China’s trade surplus really took off from 2022 onwards and the large number of 2024 is a very recent phenomenon. China’s current account surplus, that also takes into account such things as the repatriation of profits by foreign companies, was only 2.2% of GDP in 2024. US corporations make a lot of profits selling in China’s domestic economy (e.g. Apple, McDonalds, Starbucks) and keep the majority of the profits made by exporting goods from China under their own brands. Of course, the Trump administration wants to talk about that 5.6% figure, not the 2.2% figure that may draw attention to the amount of profits that US corporations are making in China.

Another issue is that during and after COVID, the US government and Federal Reserve followed massively expansionary policies. First both fiscal and monetary, and then heavily fiscal (from late 2022 when the US economy looked as if was about to roll into recession). This massive expansionary boost, given the de-industrialized nature of the US economy, naturally sucked in a huge amount of imports; including those from China and from nations utilizing Chinese inputs. The correct thing would have been to remove the punchbowl, but the exact opposite was done. An extra spur was given by the politically driven interest rate cuts in the second half of 2024, and the US Treasury Secretary’s decision to fund the US government using short-term bills in 2024; every last demand lever was pulled in 2024 as I detailed here. The Trump administration’s “Big Beautiful Bill” will just prime the pump even more, while Trump pushes the Federal Reserve for interest rate cuts.

With a Federal Government deficit of 7% stretching far out into the future, even with assumptions of continued economic growth, the US economy requires significant retrenchment not yet more pump priming. More taxes on the top 10% who provide 50% of the retail consumption within the US, heavily skewed toward imported goods, rather than yet more tax cuts for them. Tariffs will not fix this problem, unless Trump wants to see the US economy collapse into an inflationary slump that further decimates the living standards of the majority of Americans and threatens a financial crash. The problem is not Chinese under-consumption, it is US (and Western) top 10% over-consumption.

“Housing Crash” threatening a financial disaster

The Chinese government has extremely skillfully managed a controlled deflation of the domestic property bubble. A controlled deflation that may continue for a number of years, as Chinese nominal incomes keep increasing by perhaps 7% per year, to bring house prices into a reasonable level with respect to incomes. At the same time, there has been an astonishing reorientation of investment from property into the productive forces. A reorientation that is only just starting to play out in the technological upgrading and advancement of Chinese society. While the US and Western top 10% over consume and grant themselves more tax cuts, the Chinese Party-state drives an acceleration in the growth and development of the productive forces.

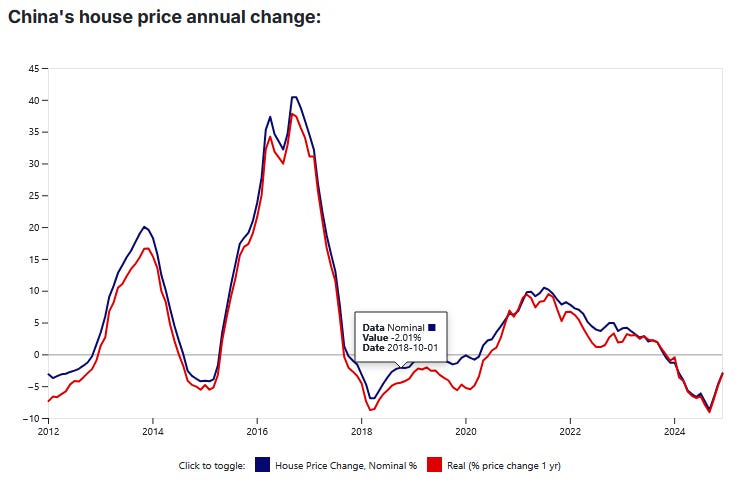

Below, from Ian Welsh’s web site, is a graph of Chinese house price inflation in which can be seen the 2012-2014 bubble and then the much bigger 2016-2018 bubble. The red line adjusts for inflation, but not growth in incomes that were very rapidly increasing during this period. Prices corrected in the 2018-2020 period but then bounced back somewhat from mid 2020 into early 2022. Then they stabilized and started to fall from late 2023 onwards. If the Party-state maintains nominally falling to flat house prices over the next decade they will have halved house prices in terms of average income multiples. A controlled relative deflation that will not threaten financial stability but will greatly benefit the younger generations.

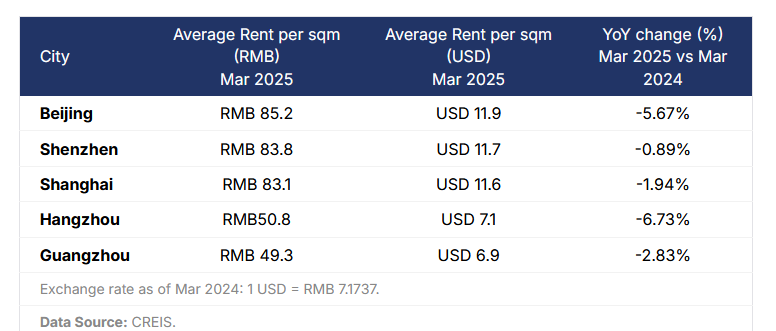

Rents increased much more slowly than house prices, and have most recently started falling. This is great news for younger generations that tend to be the greatest renters and have lower incomes. With their propensity to spend the incremental Yuan much higher than more well off older generations, lower rents rapidly turn into higher consumption; as noted retail consumption is strongly increasing. Again, from Ian Welsh’s site:

100 square metres is about the same as 1,000 square feet, which means that in Beijing a 1,000 square foot apartment can be rented for the equivalent of USD 1,190 per month. That’s in the most expensive rental market in China, where the annual average salary is about US$26,100 per year at market exchange rates. The same sized apartment would be more than US$4,000 per month in New York City, where the average annual salary is about US$80,000. The average annual salary in NYC is 3.1 times higher than Beijing, but rents are at least 3.36 times higher; with rents falling and incomes rising much faster in Beijing. In Guangzhou, in the heart of the southern high tech conurbation, average annual salaries are close to US$22,000 per year while the average monthly rent is only US$690 per month for a 1,000 square foot apartment.

As Mr. Welsh succinctly puts it:

You can’t be an industrial power if rentiers: people who expect to make money thru time arbitrage and managed scarcity, are in charge of your society … Anyway, China needs to keep housing and rental prices down. At the very least they need to increase less than wage increases and for many years. All signs are, that as is most often the case, the CCP [sic] is succeeding at the policy goals it set out for itself.

“Deflation” threatening a financial disaster

Its called actual market competition and sustainable monetary and fiscal policies that align with the growth in the economy. The exact opposite of the pump-primed highly concentrated oligopolistic, corrupt, and financialized rentier economy of the US, where corporations took advantage of the COVID supply disruptions to massively increase their profit margins while in many cases shitifying their products and services. When the economy is growing at 5% year, mild deflation is not an issue and may in fact represent large leaps in productivity and highly competitive markets. That is what China is experiencing. For example in an EV market that is both growing at 30% per year and experiencing falling prices.

“Autocratic” state unable to compete with the flexible “democracies”

The Western nations are oligarchies, dominated by a small elite which utilizes utterly performative “democratic” processes to hide and obfuscate their power. As the most purely bourgeois elite dominated society, the US is the most advanced in this respect with even money defined as protected “free speech”. These oligarchies if anything have shown themselves to be both inflexible and incompetent. In contrast, the Chinese Party-state has shown a great deal of flexibility, and uses highly competitive domestic markets to drive a high level of corporate responsiveness, while engaging in extensive discussions with the citizenry before setting policies. In the West there is also little if any impact for state officials and politicians when they fail, with many seeming to “fail upwards”; such as Ursula von der Leyen. In China, officials are quite open to consequences from public criticism and policy failures. The legitimacy of the Chines Party-state among the domestic population is many times higher than that of the US state and politicians among the US population.

“Demographic Time Bomb”

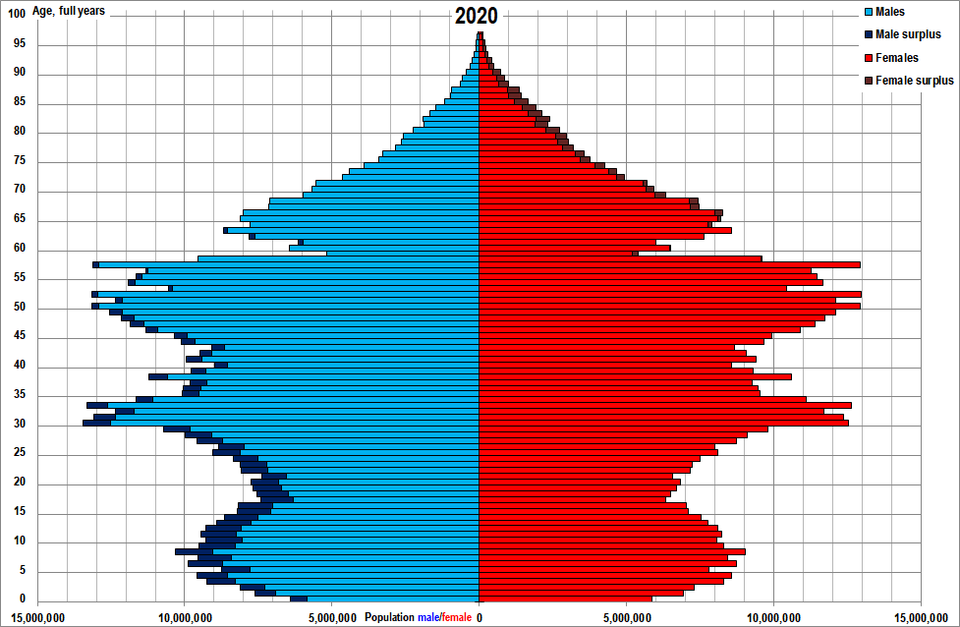

Anyone who uses this type of concern trolling has not even looked at the Wikipedia Chinese demographics page. From that it can very clearly be seen that the Chinese working age demographic (18-60) will not be collapsing any time soon. In fact if we take the 2020 demographic chart below and move it on 15 years to 2035, we will see that one of the most productive age groups (45-50) will actually increase while the number of new recent entrants to the workforce (20-35) will have also increased. Only the 30-45 year old and 50-60 year old age groups will have decreased.

There is also still some room still left for the movement of workers from rural occupations to the big cities, with the Chinese urbanization rate of 67% compared to over 80% in the US and Western Europe. In addition, technologies such as exoskeletons and robotics can help older workers maintain their productivity. The Chinese younger generations are also very well educated, significantly better than their elders, and fit and healthy. Unlike in the West, where educational levels have declined and a significant share of the younger generations are either unfit, unhealthy, or both. Given also the redirection of resources away from property investment and towards the productive forces in China, ongoing GDP per capita increases of 5% are quite possible into the mid-2030s and beyond.

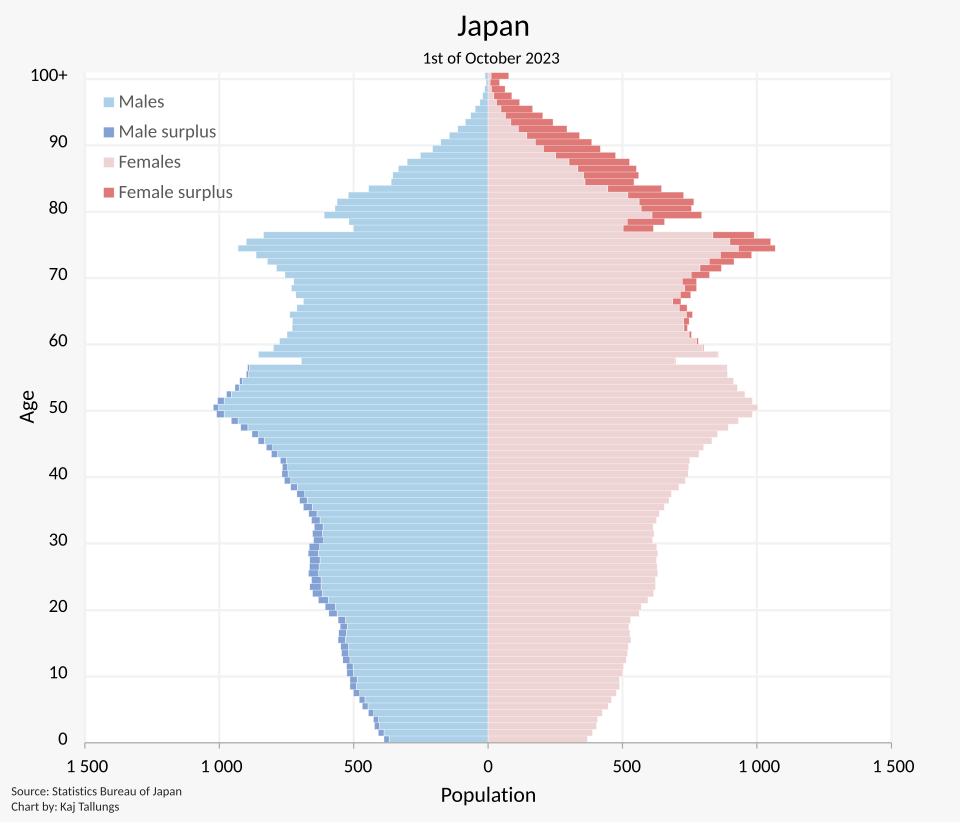

Unlike a Japan that faces a very real immediate demographics issue, combined with the Chinese and US assaults upon its productive forces.

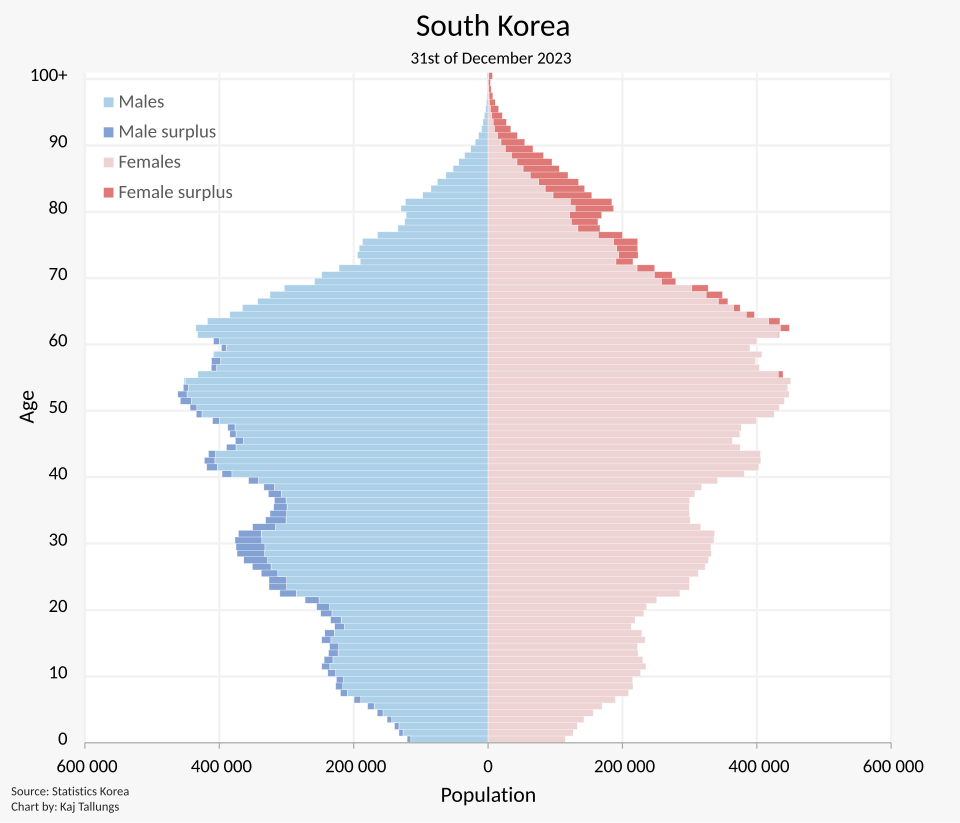

And a South Korea which will face a major demographic issue in the 2030s.

Progress but “At What Cost”

When all else fails, Western mainstream journalists search for any negative that they can offset against Chinese progress. So that they can say “yes, China is being so successful but at what cost”. This is the end game of the failure of the Western propaganda.

Of course China is not perfect, no nation will ever be perfect; most especially one of 1.4 billion people. But it is lead by the Party-state in a far superior way to the leaderships of the West, especially from the point of view of the vast majority of the population. That is why the Party-state enjoys extremely high levels of social legitimacy, levels only dreamt of by Western leaderships. You would of course not know much about this watching, reading and listening to official Western media, state actors, and courtiercommentators.

I was recently invited to a closed door consultation event at the Chinese Embassy in Ottawa which of course I cannot write about. But there is one thing that struck me that I will mention, and that was the attitude of the extremely professional Chinese diplomatic staff. I would liken it to a “mild exasperation” covered expertly by a fastidious diplomatic approach. It struck me that diplomatic members of the Chinese Party-state sometimes must feel like they have come across some unfortunate person that they are happy to help out but are then regaled with the complaints of the hapless person about their own supposed shortcomings. The proposals of win-win solutions from the much bigger and stronger person to the much smaller and weaker unfortunate being met generally with a residual arrogance from the times when the roles were reversed. The reality is that China is just fine thank you, and it is the West that needs to learn a lot more humility and self-awareness for its own good and the good of humanity in general.

Instead, China being just fine thank you is what is driving Western oligarch aggression and dark propaganda against China. The Western oligarchy sees its global dominance slipping away in the face of a more successful state/society complex that does not allow for a bourgeois oligarchy. The Chinese Party-state may be fine with the Chinese saying of “to get rich is glorious” but only when the rich do not attempt to use their wealth to usurp the Party-state that serves the national good. Profit levels are significantly lower in China because the Party-state makes sure that there is real competition within markets, and that corporations orient themselves toward value creation rather than rent seeking behaviours. With the home of the greatest rent seeking, the financial sector, kept under very firm state control. China threatens both Western global hegemony through its continued economic growth, and provides the “threat of the good example” (as Chomsky put it) that is a direct threat to the legitimacy and sustainability of the Western domestic oligarch dominance. So instead, a constant stream of lies will be propagated by the corrupted officials and organic intellectuals of the Western states, the bought and paid for Western political actors, and the Western media that is controlled by an incredibly small group of oligarchs and their tools.

Humility and self-awareness do not come easily to those that have ruled for centuries, and see their civilizational primacy as a natural and unchangeable reality that has nothing to learn from the “lesser” civilizations. Such pride comes before a fall as the saying goes, just as the Qing rulers found out in the early nineteenth century.