Trump Accelerates The Decline Of Western Vehicle Manufacturing, And Much More

Surrendering The EV Supply Chain To China

National power is predominantly based upon the relative scale and technological advancement of the productive forces of a society; a reality that is accepted by pretty much all branches of international relations scholarship. Vehicle manufacturing is the most advanced example of the mass manufacturing of highly complex products that utilizes huge supply chain logistics. It is also the greatest user of machine tools, robotics, embedded software, electric batteries (for electric vehicles), electronics, electric motors (for electric vehicles), hyper-efficient internal combustion engine technology (for plug in hybrids) and the outputs of many other industrial sectors. For example, one third of all machine tools in the world are used directly in the automotive sector; and that sector tends to be contain many of the leading edge applications. With the Military Industrial Complex (MIC) heavily dependent upon the health of the domestic civilian vehicle industry.

To lose the car industry is the national industrial equivalent of a heart attack, with the survival of the rest of the manufacturing body highly questionable. This is the prospect facing the Western industrial sectors, as the Chinese car industry has been able to utilize electric vehicle technology to leapfrog the Western industry’s lead in the highly complex area of internal combustion engine (ICE) technology; replacing the ICE with a many times simpler electric drivetrain obviates the West’s lead in ICE technology. Even the hyper-efficient internal combustion engine technology used on PHEVs is much more a product of electronic management systems and the ability to run the ICE at a constant high efficiency rpm as it supplies power to a battery rather than directly to the powertrain. With a focused multi-decade effort on building a fully domestic electric vehicle supply chain, China is now accelerating its takeover of global vehicle production.

At this very time, the Trump administration has decided to take the US out of the EV game, through the removal of the ZEV (zero emission vehicle) mandate incentives, and the EV purchase incentives (US$7,500 for a BEV and US$3,750 for a PHEV). Adding to this, the Canadian government also removed its EV incentives, and the US administration even put on hold plans to fund more EV charging stations. The share of EV’s will most probably fall from its current 8% market share to the 6% level or lower in the next year or so; after the Q3 2025 last-minute rush.

In China, we are seeing the promise of electric vehicles being fulfilled; a new technology segment with lots more technology innovation and cost efficiency to be wrung out of it. The prices have now crossed below those of ICEVs and will keep falling, utterly invalidating the ICEV technology in the market place. The US has now built a wall between itself and this huge innovative space.

The biggest loser will be a Tesla that domestically produces all of the cars it sells in the US. It will have a long-term lower level of profitability and sales, negatively impacting US vehicle production. The same will go for smaller BEV players such as Rivian and Lucid, as well as the EV sales of the bigger players. The US market will become a specialist ICEV market while the rest of the world is moving to EVs. Both domestic and foreign producers will have little incentive to build new EV production capacity in the US due to the low level of sales and the lack of development of the EV supply chain. Better to build that capacity in a China with the largest by far EV market and the largest and most developed EV supply chain.

This is already true of many foreign brands, which use China as an export base to Asia, South America and MENA etc. At the same time of course, the Western car brands that lag so far in EVs are being forced out of the Chinese market; one that provides a significant amount of their sales. In 2024 these brands sold many millions of cars in China, and are set to lose much of their global sales (30% for VW, BMW and Mercedes, 25% for Honda, 20% for Nissan, 15% for Toyota and Porsche).

VW: 2.93 million (out of 9.03 million globally)

Toyota: 1.78 million (out of 10.8 million globally)

Honda: 852,000 (out of 3.75 million globally)

BMW: 715,000 (out of 2.45 million globally)

Nissan: 696,000 (out of 3.35 million globally)

Mercedes: 684,000 (out of 2.39 million globally)

Porsche: 56,877 (out of 310,718 globally)

In an attempt to survive in the Chinese market the foreign brands are becoming increasingly dependent upon Chinese batteries, Chinese electric motors, Chinese advanced driver assist software (ADAS) and many other Chinese components. In some cases the foreign brand cars are little more than rebranded versions of Chinese brand vehicles. A good example is Audi in China, which is going full-in with its local production partner SAIC and its China-specific brand of AUDI utilizing SAIC BEV platforms, Momenta ADAS, and CATL batteries. The first model, the AUDI E5 Sportback BEV sedan is on pre-sale for only RMB 235,900 (Euro 28,200); an equivalent Audi A5 ICEV starts at Euro 45,200 in Germany.

Other examples are the Mazda EZ-60, a re-skinned Changan vehicle.

The Toyota BZ5 made by FAW, with BYD batteries and electric motor, Momenta ADAS.

And the Nissan N7, which a re-skinned Dongfeng vehicle.

Nissan has already announced that it will be exporting the N7 from China, and many of these cars could become an “all markets outside Europe and North America” brand, greatly retarding the development of EV technology within the home country (Germany and Japan) and of course, the US.

To add insult to injury, the US has forced unequal trade agreements upon Japan, South Korea and the EU which include 15% tariffs on car imports. The German brands, and some of the Japanese brands (e.g. Subaru), still supply a significant chunk of their sales from imports of components and whole vehicles from their home countries. In 2025, the German brands are set to lose Euro 10 billion in cash flow due to the US tariffs. Mercedes cash flow is forecast to fall from US$11 billion in 2024 to only US$3 billion this year, VW from US$9.5 billion to US$3.8 billion, and BMW will see a small fall. The foreign manufacturers are now incentivized to move ICEV production to the US from Europe by the 15% tariff together with lower energy prices, lower wages and non-union workforces.

Another problem is the highly integrated North American vehicle market where there is substantial production in Canada and Mexico (about 3.5 million vehicles) that is destined for the US, and visa versa on a smaller scale. Mexico and Canada may have exemptions to tariffs for the large amount of US-produced parts in vehicles produced there, but the effective tariff rate is still in the region of 10-15%. The Japanese and German manufacturers, as well as the US “big three”, have substantial manufacturing plants in Canada and Mexico. For example, BMW manufactures the 2-series and 3-series sedans in Mexico.

The Japanese manufacturers (excluding Toyota) will become even more split between a US market supplied from their factories in that country that predominantly produce ICEVs, and a highly protected home market. Hyundai-Kia and Toyota do have very significant sales in Europe and the rest of the world; both of which are moving to EVs. The German luxury vehicle manufacturers of Audi (part of VW), BMW and Mercedes will face a much more existential crisis as they see major drops in their China sales, reduced profitability within a US focused on ICEVs and disruption within their manufacturing supply chains. Their exports from the US will be affected by the new US tariffs on steel, aluminum and copper. For the main VW brand, the US sales of 380,000 are a relatively small share of its global sales and will be ICEV-focused as the company moves toward an EV future elsewhere. With respect to a Porsche that imports all of its cars from Germany, the head of VW has stated that it:

was being squeezed by a “sandwich” of tariffs and a weak Chinese market.

Of course, the Chinese market is only “weak” with respect to the highly over-priced German vehicles from the likes of Mercedes, BMW, Audi and Porsche that are imported from high cost Germany; exacerbated by the Chinese government’s reduction in the cut-off of the 10% luxury car tax from RMB 1.3 million to RMB 900,000. In my next quarterly update on the global car industry I will be focusing in on the assault of so many Chinese brands upon the luxury and super-luxury end of the market, even causing problems for some of the established Chinese luxury car brands.

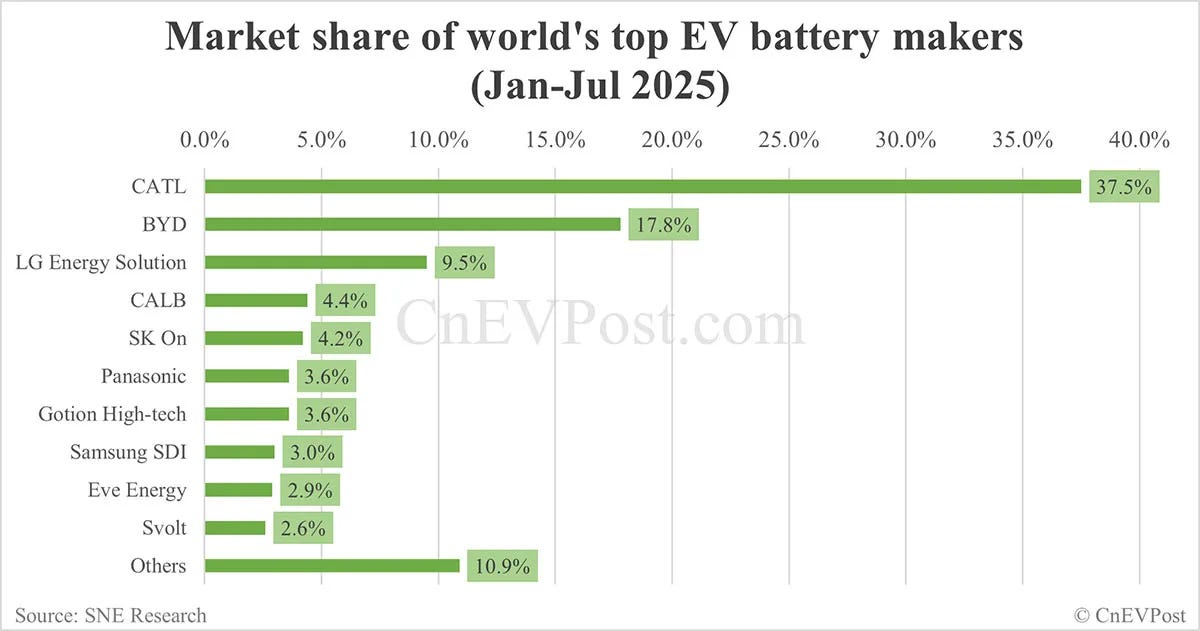

The Chinese brands can focus on the drive toward EVs given the dynamic of the Chinese market, and their increasing successes selling EVs abroad. This includes in Europe, and not just in a UK that sits outside the EU anti-China EV tariff wall. The Chinese EV supply chain is utterly dominant and will now become even more so. The Chinese EV battery manufacturing companies already have an utterly dominant position in the global market, and an overwhelming one in the Chinese market. Every company below except for LG, SK On, Samsung SDI and Panasonic is Chinese. Volume grew 35.3% y-o-y. CATL grew 34%, BYD 52%, while LG only grew 9%, and the Chinese CALB was the #4 in market share.

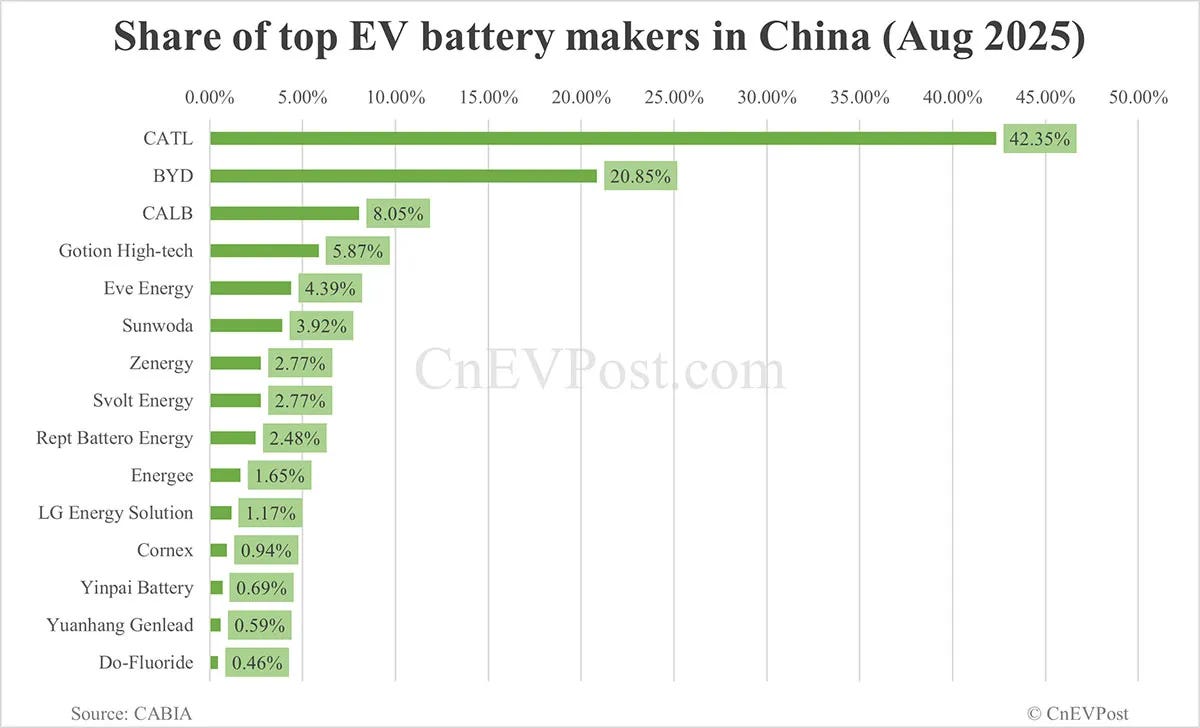

Every company below except for LG is Chinese, and the Chinese market is growing at 32.4% per year. The Chinese market is two thirds of the global market.

Even the smaller Eve Energy is leveraging its EV battery business to produce solid state batteries for robots and flying cars (yes you read that right) in 2025, with solid state batteries for hybrid light vehicles planned for 2026. The company has the same production scale as Samsung SDI while being concentrated in the most dynamic market. In China, LG is focused on the declining market share ternary battery segment, rather than the now dominant and and faster growing LFP battery sector.

At the same time, Chinese companies are increasingly sourcing the chips and other electronics they use from Chinese suppliers. BYD already manufactures a lot of the electronics in its cars itself, and companies aligned with Huawei have access to its huge electronics manufacturing and software capabilities. Recently, even the likes of Xpeng and Nio have developed their own Advanced Driving Assistance System (ADAS) chips. Xiaomi is also in the process of developing its own ADAS chips. Additionally, the Chinese vehicle manufacturers are the largest users of robotics and machine tools in general, nearly all sourced from Chinese manufacturers.

Momenta, the leading independent ADAS provider in China, is being used by more and more of the foreign brands and is now partnering with Uber in Germany with respect to autonomous vehicles. The world’s largest LiDAR sensor manufacturer is Chinese, Hesai Group. In 2024 it grew sales 126% to 501,900, and projects sales of between 1.2 million and 1.5 million in 2025. It provides LiDAR units to the likes of Li Auto, Zeekr, Leapmotor and Xiaomi. The production of integrated vision systems for cars is also dominated by Chinese producers.

The US market may be protected by the 100% plus anti-China EV tariff wall, but its supply chains will continuously fall behind the Chinese supply chains and lose the sales that they currently make to the Chinese vehicle manufacturers; becoming perhaps an EV and car electronics equivalent of the now defunct German Democratic Republic (GDR). With it will go the myriad of defence industries that rely on a healthy and globally competitive automotive manufacturing sector and the supply chains that exist because of that automotive industry. The ability of the US to wage war will be severely attenuated, while the capabilities of China will keep on increasing.

While damaging the productive forces of Germany, Japan, South Korea, Canada and Mexico, the US will also be damaging its own productive forces and national power. The US empire will be weakened as a whole, and even at its core. With such a weakened set of European, Japanese, South Korean and Canadian vassals the US Empire will take on a much less impressive hue. With many, including Mexico and even South Korea and Japan looking at China in a more positive light. Trump continues to show himself to be a wrecking ball for the US Empire, too wound up in short term profiteering for his oligarch colleagues and win-lose propositions for what may start to become his erstwhile allies/vassals; more it seems in Asia than in the still utterly subservient Europe.